UX Design Challenge

Design One-Stop Shop for SBI

SBI ONE

Rounds of iterations

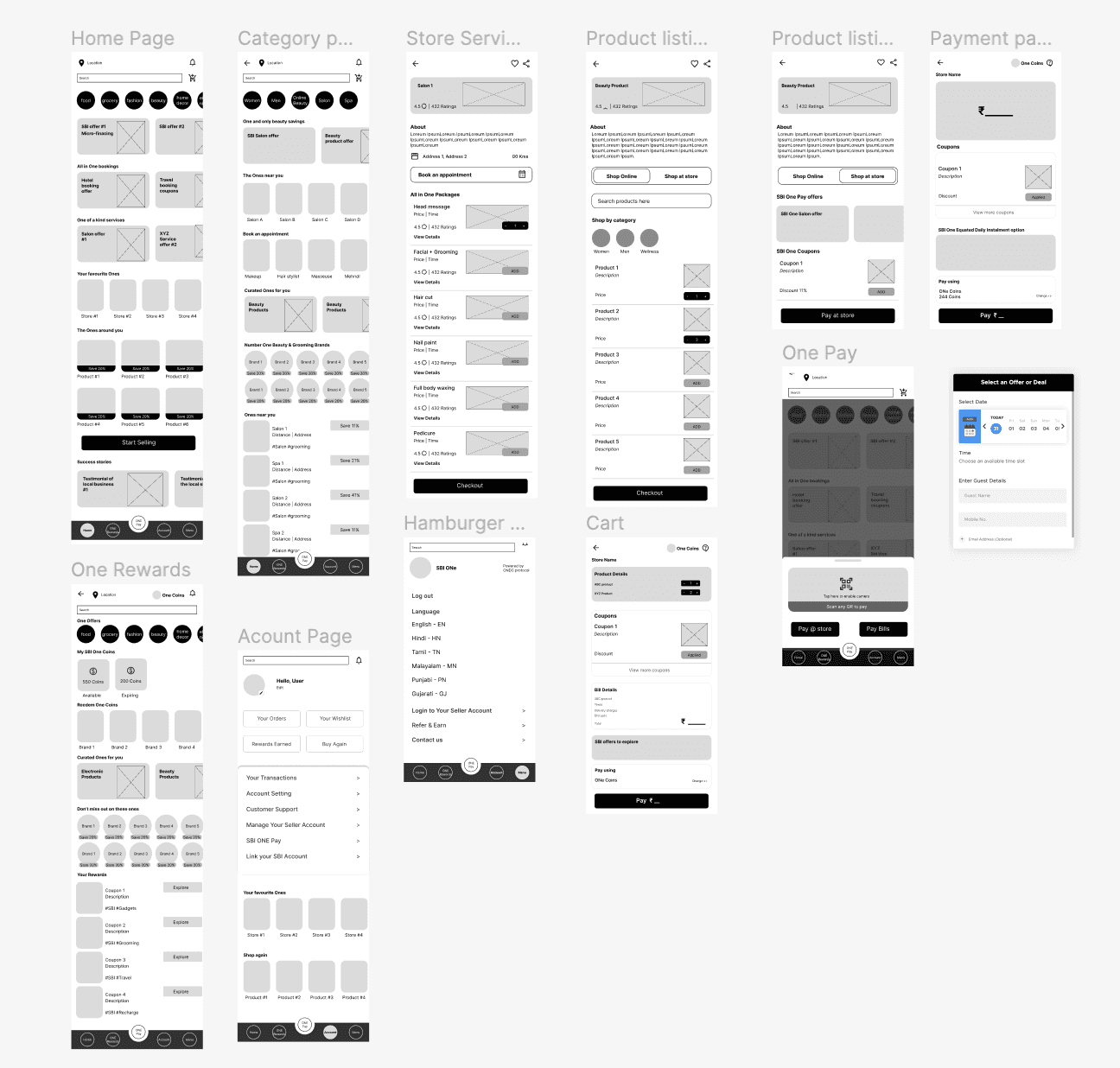

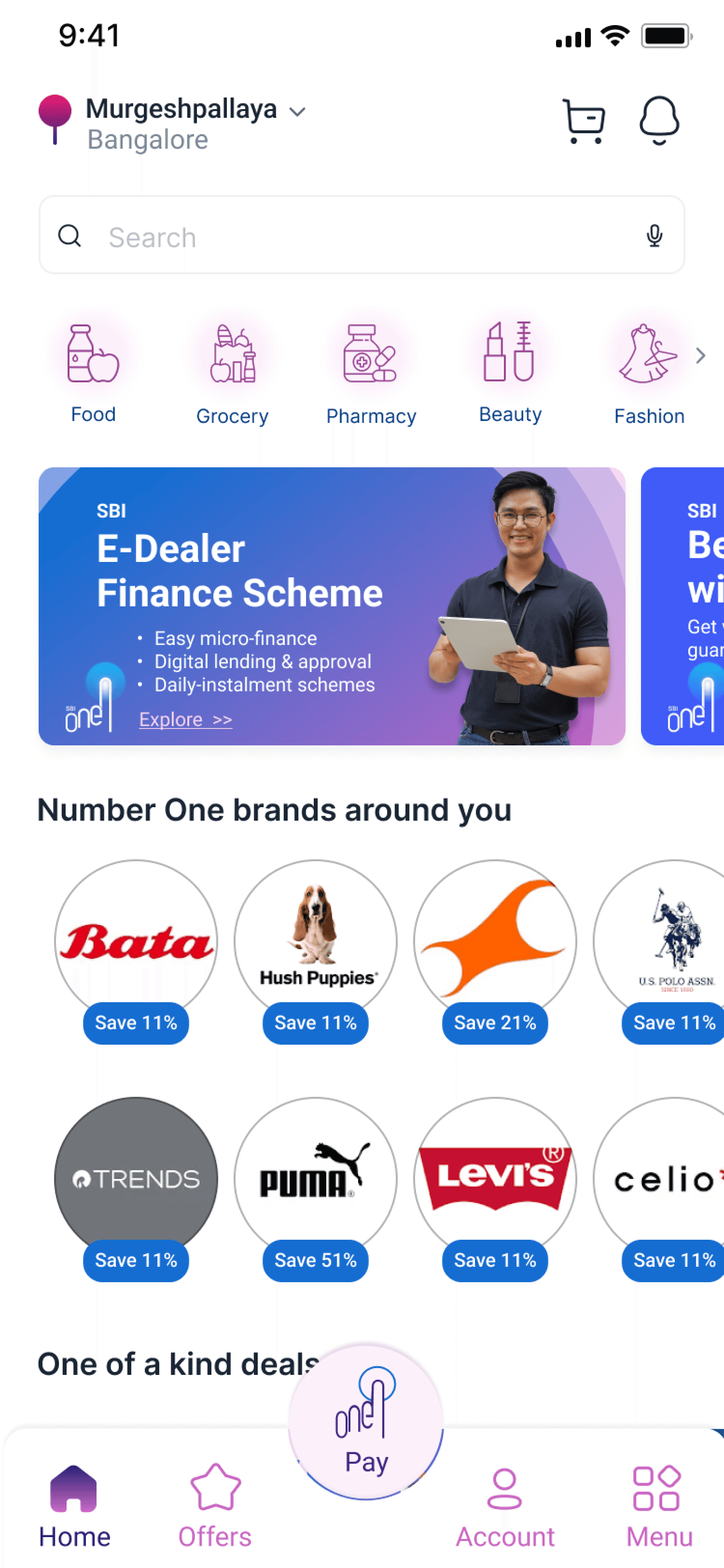

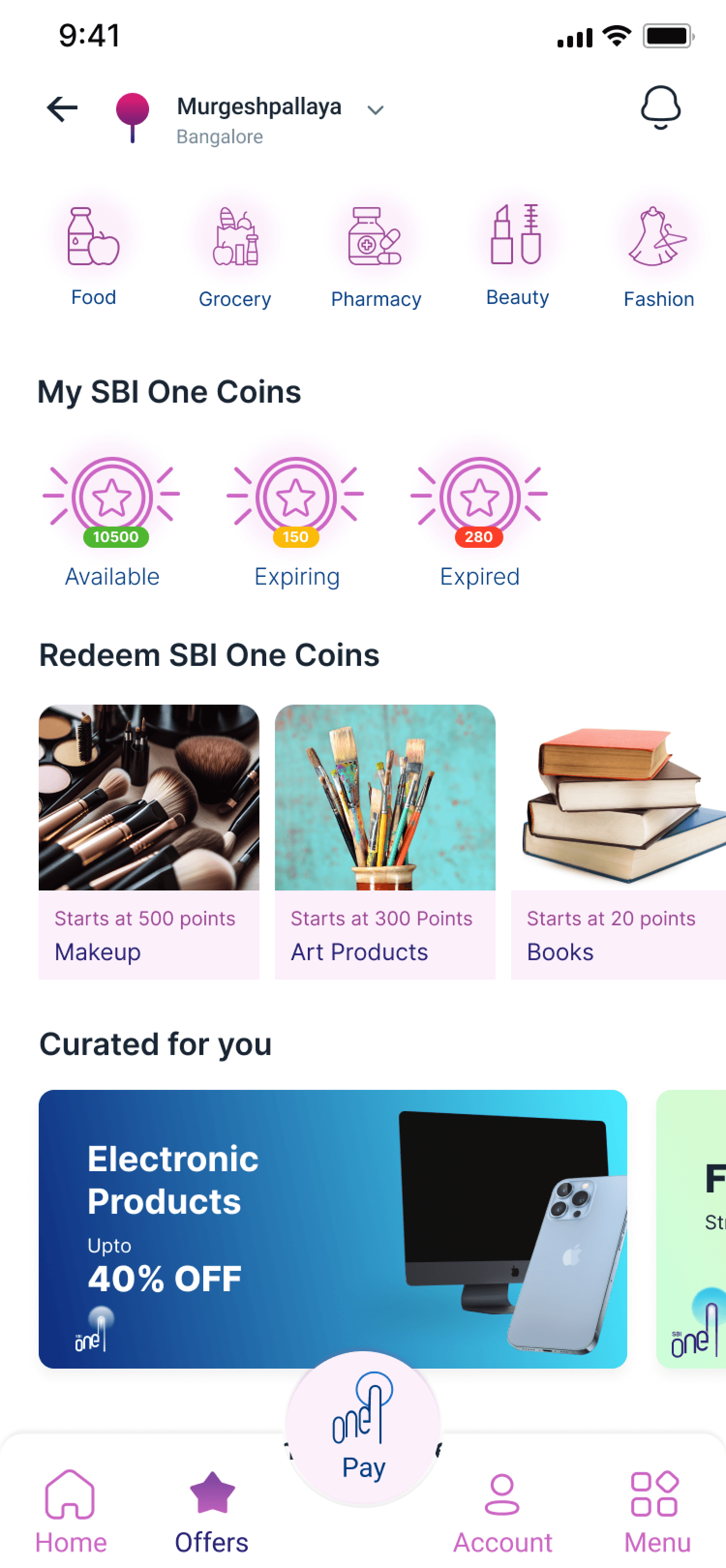

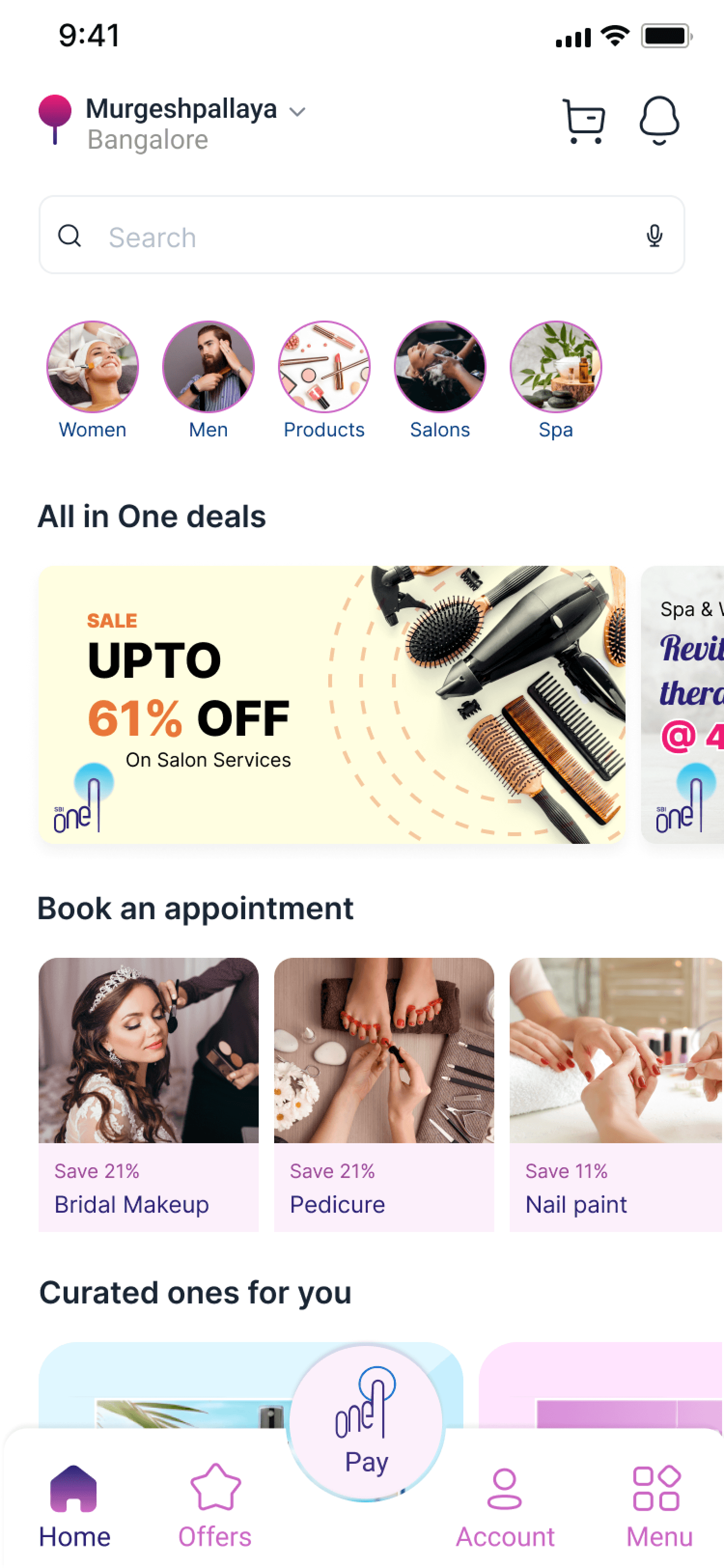

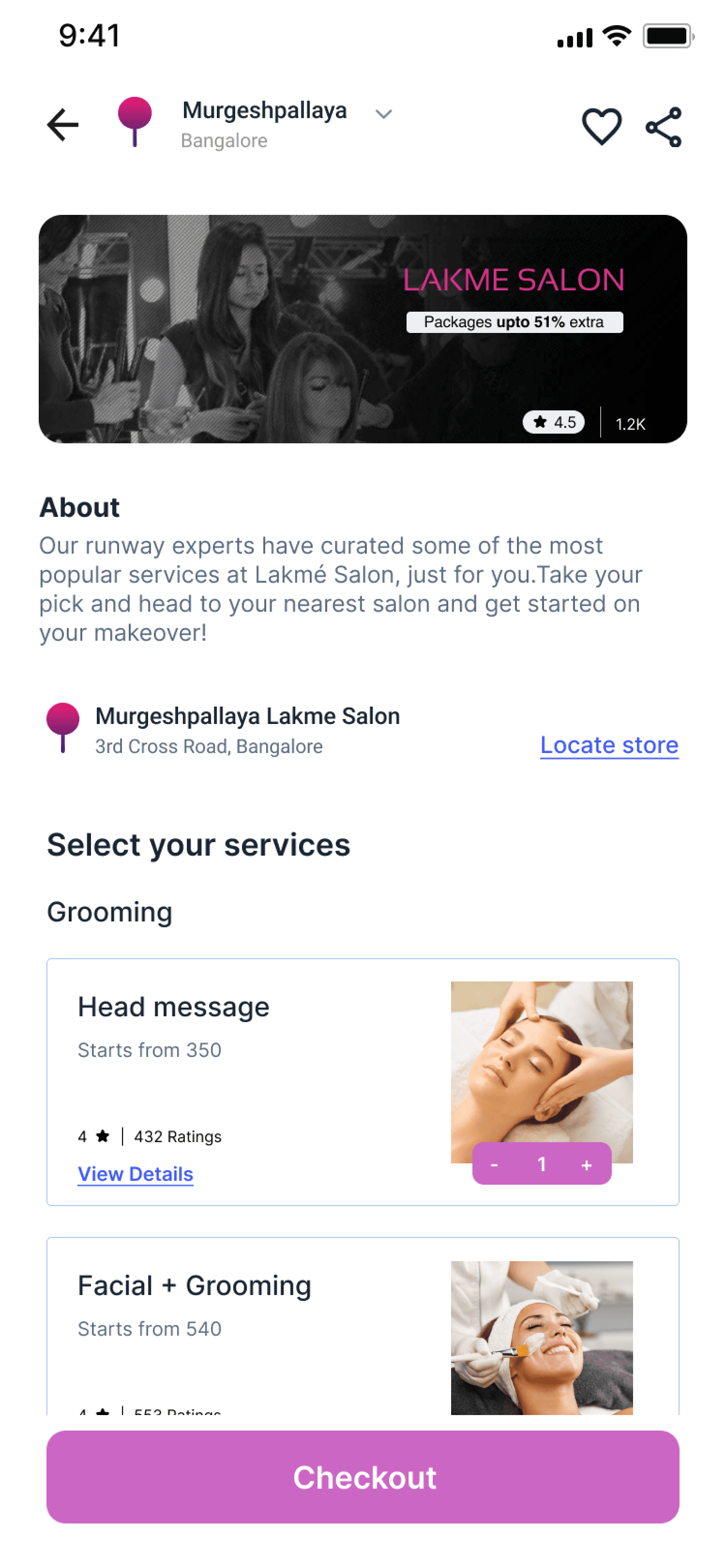

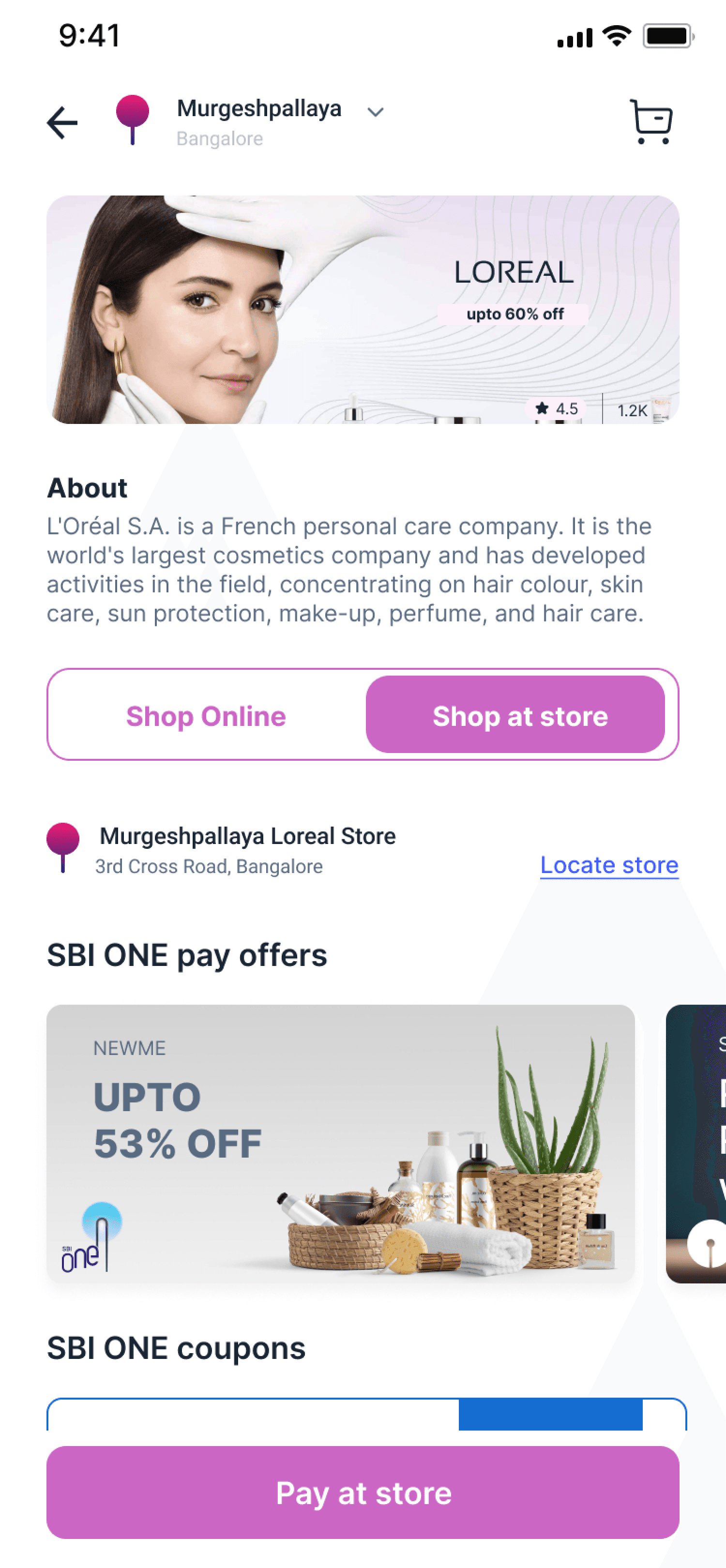

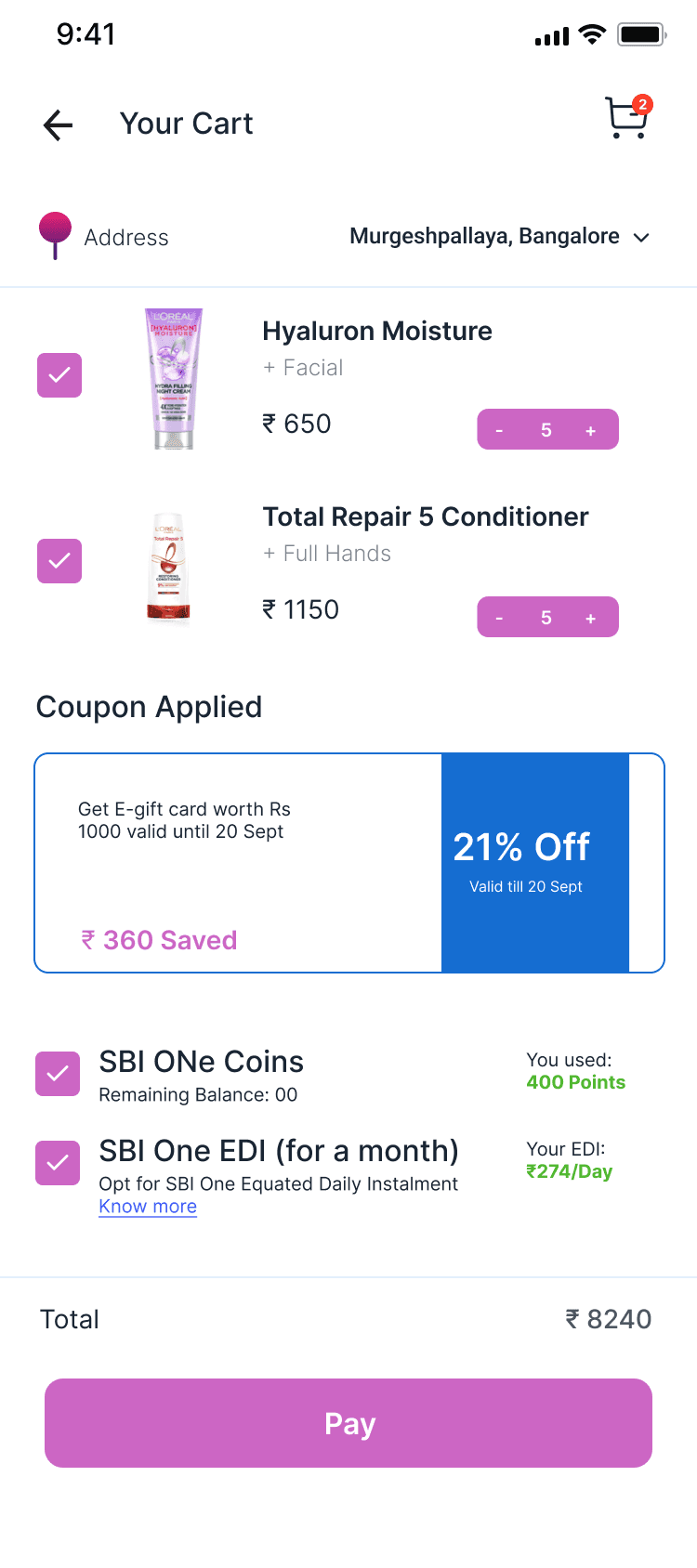

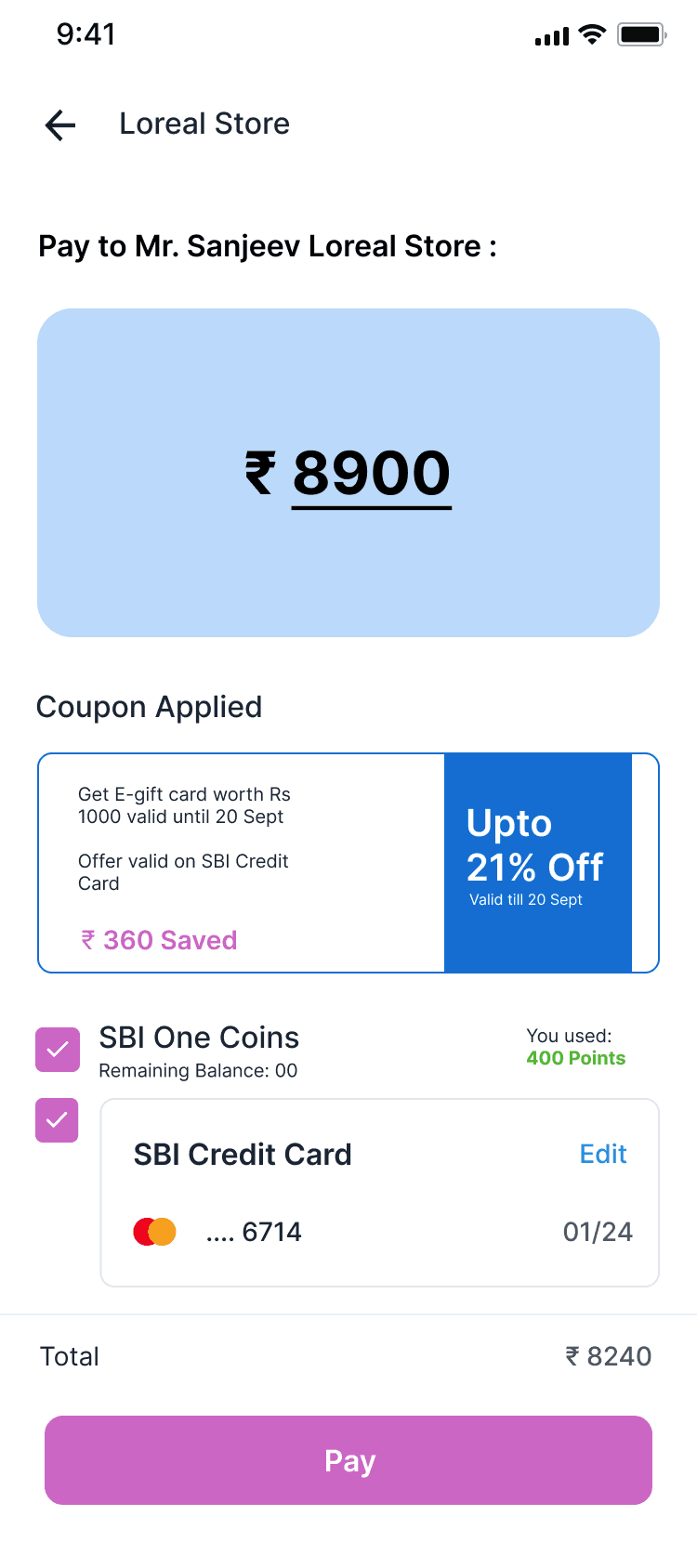

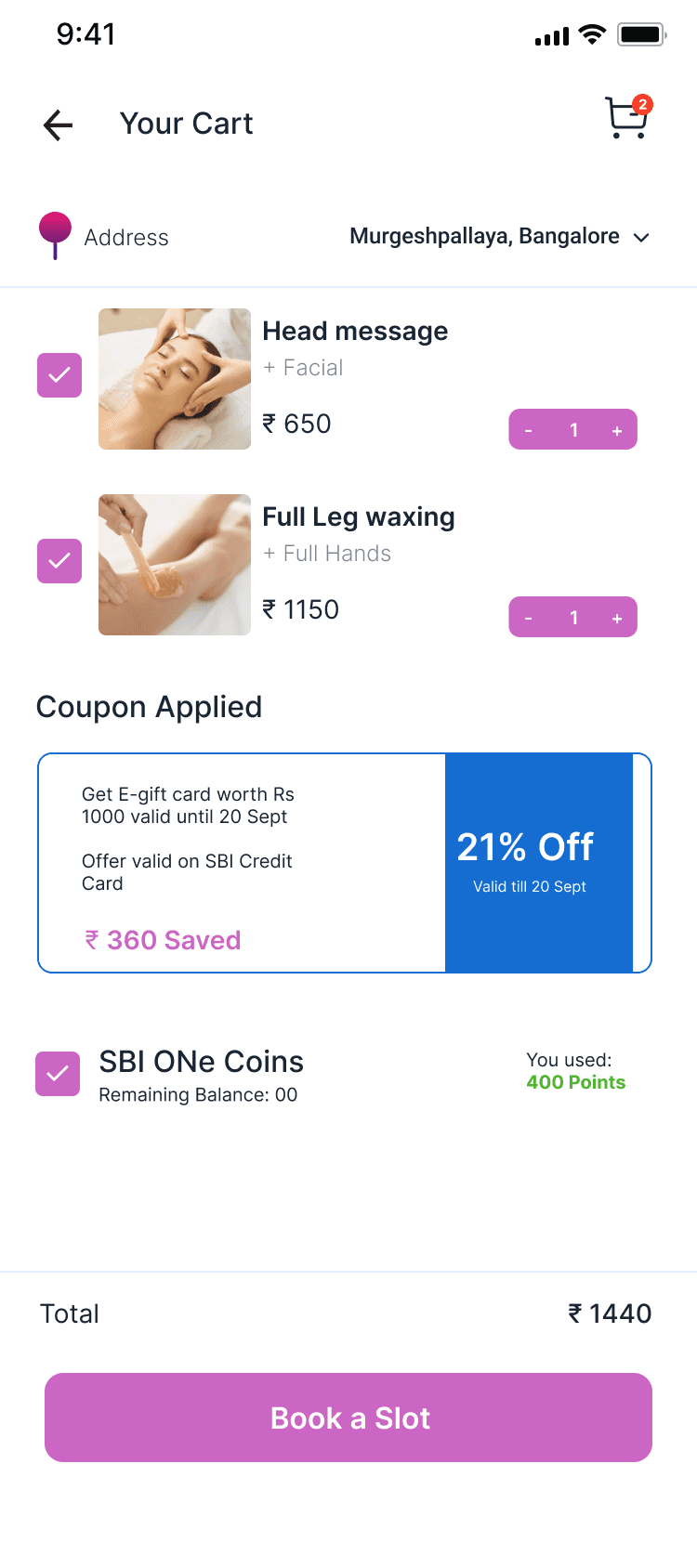

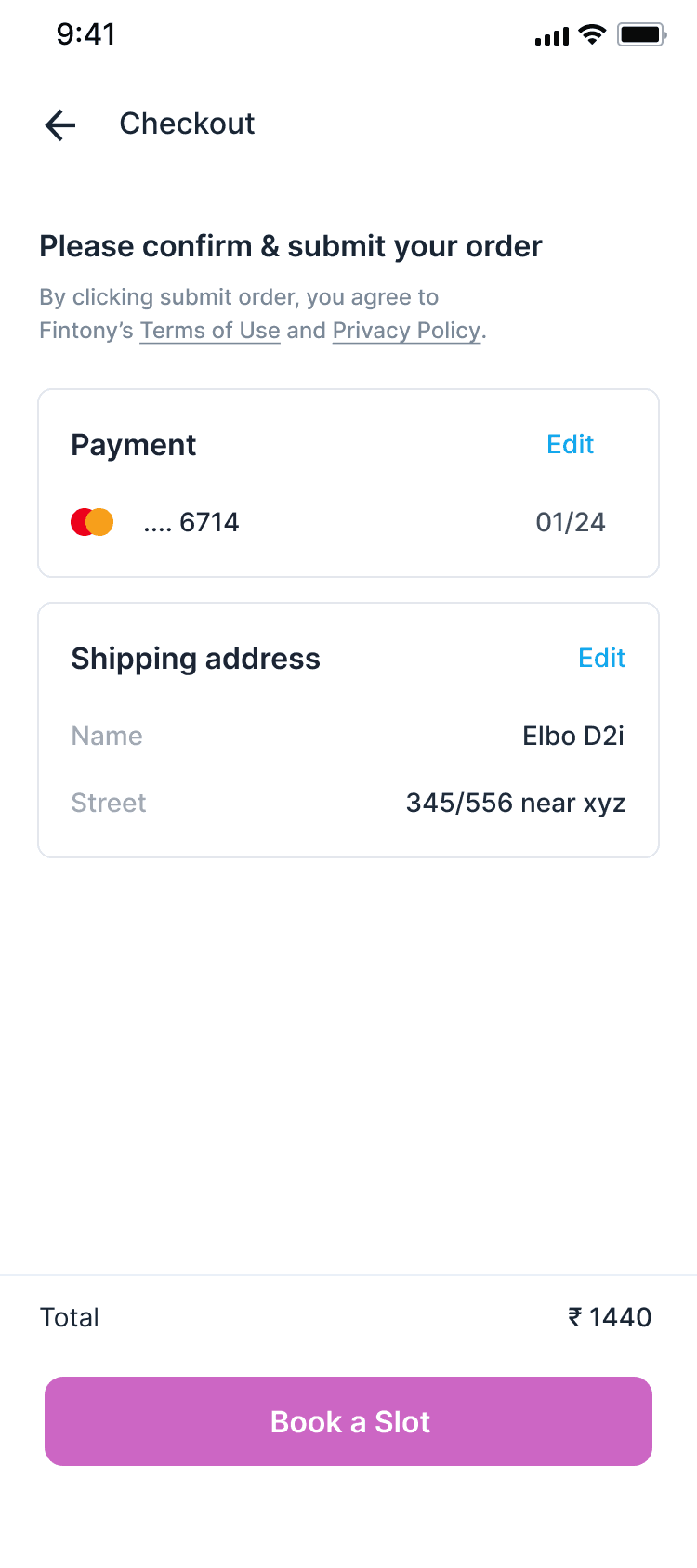

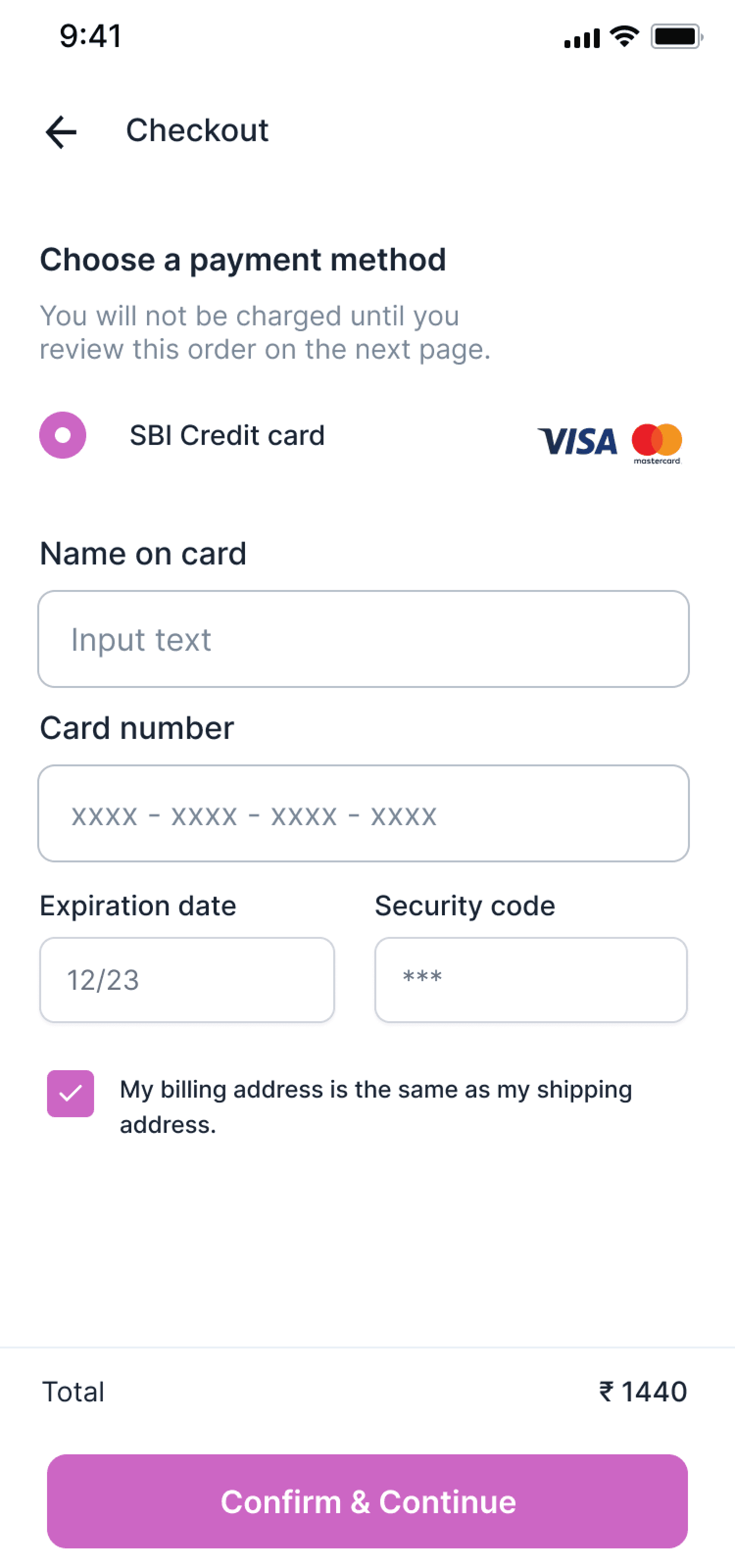

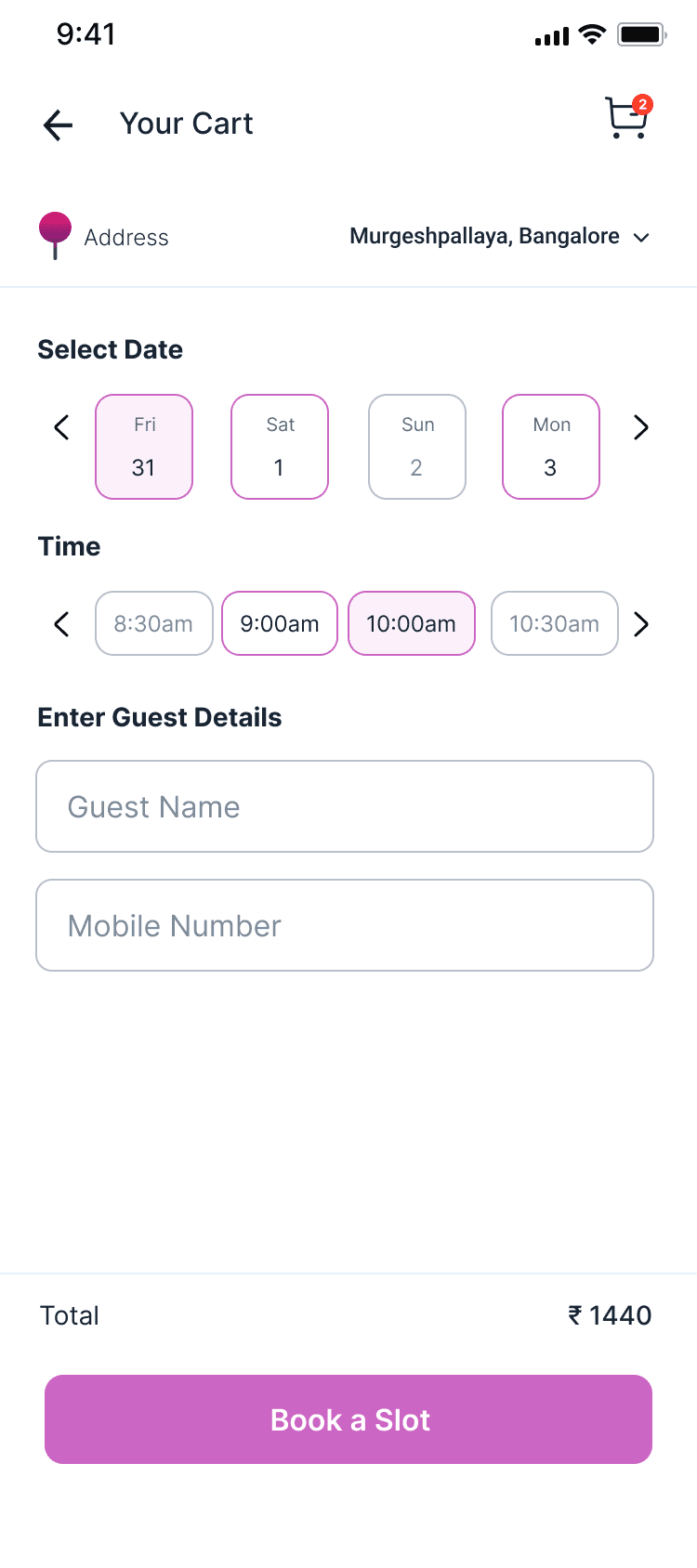

Here are some of the Hi-Fidelity Wireframes we designed

The Problem Statement

How might we help SBI create an aggregator platform that include local shops as well so that customers mend to all their shopping needs from a single platform and benefit from the discounts and coupons provided by SBI?

Project Goals

Create an aggregator platform for seamless shopping experience

Motivate local businesses by providing them digital platform

One-stop solution for banking and shopping needs.

Our Process

My Role and Contribution

In my role, I began with research to understand competitors, followed by conducting user interviews and stakeholder mapping. After completing both qualitative and quantitative research, I designed personas. I then contributed to the "to-be" journey and conceptualized ideas and wireframes. Additionally, I contributed to the User Interface design for the app.

Define

Discover

Ideate

Design

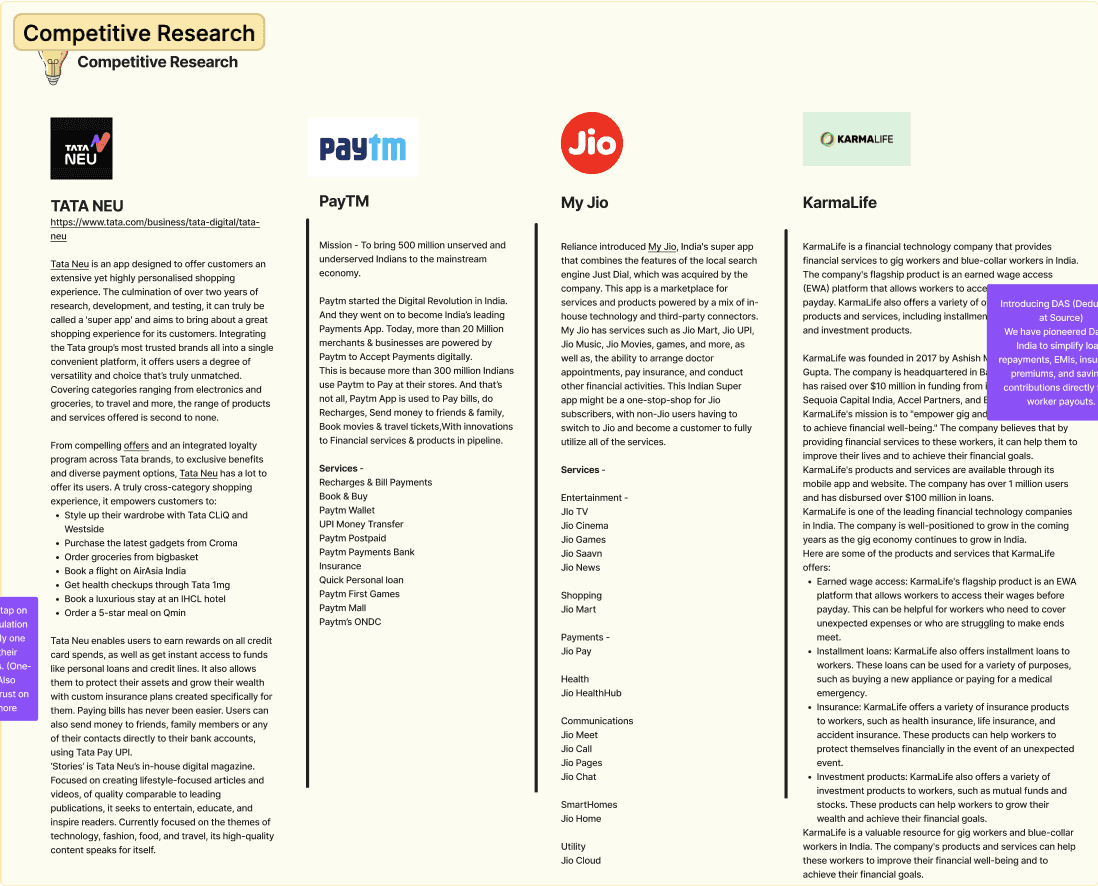

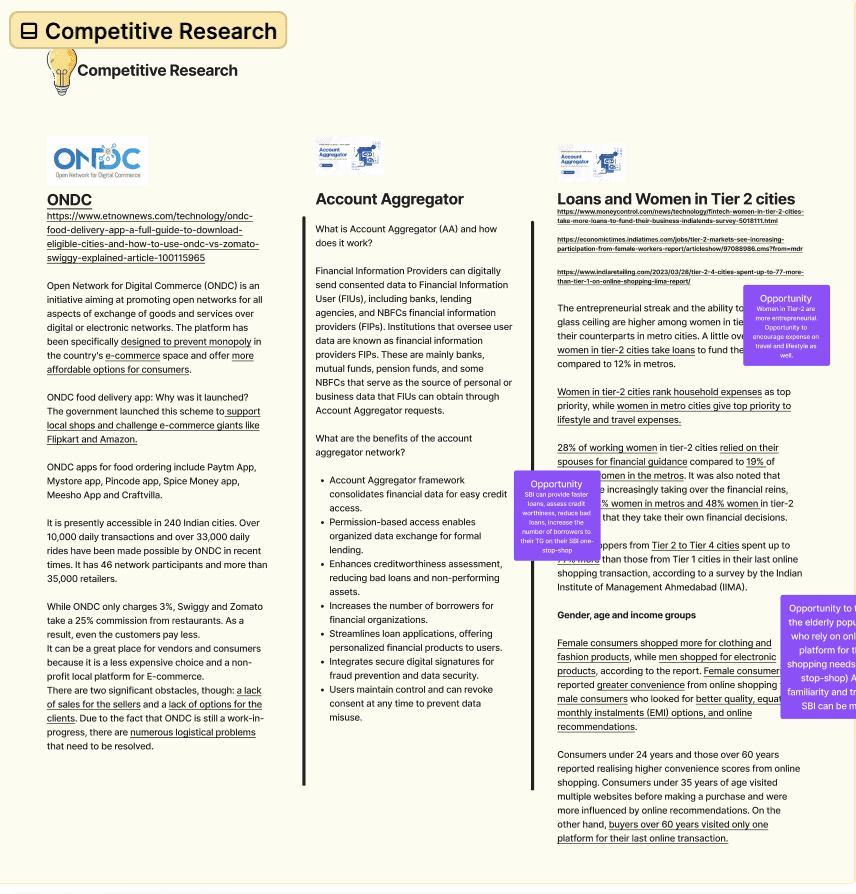

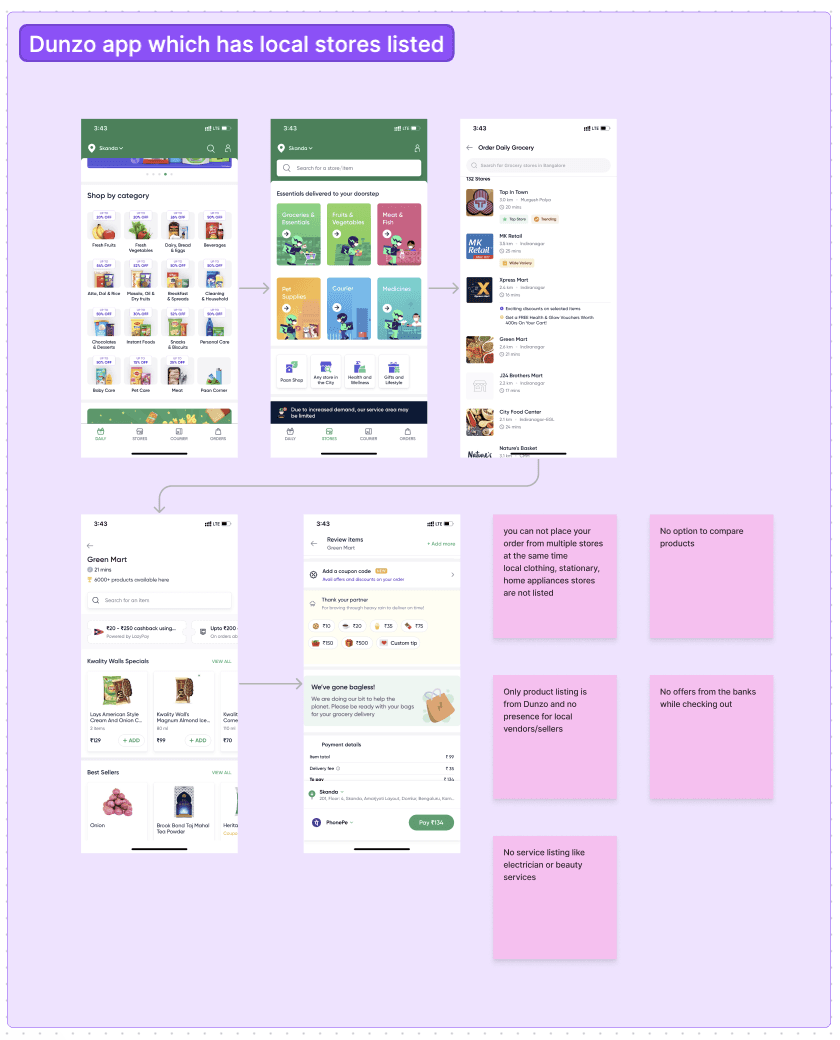

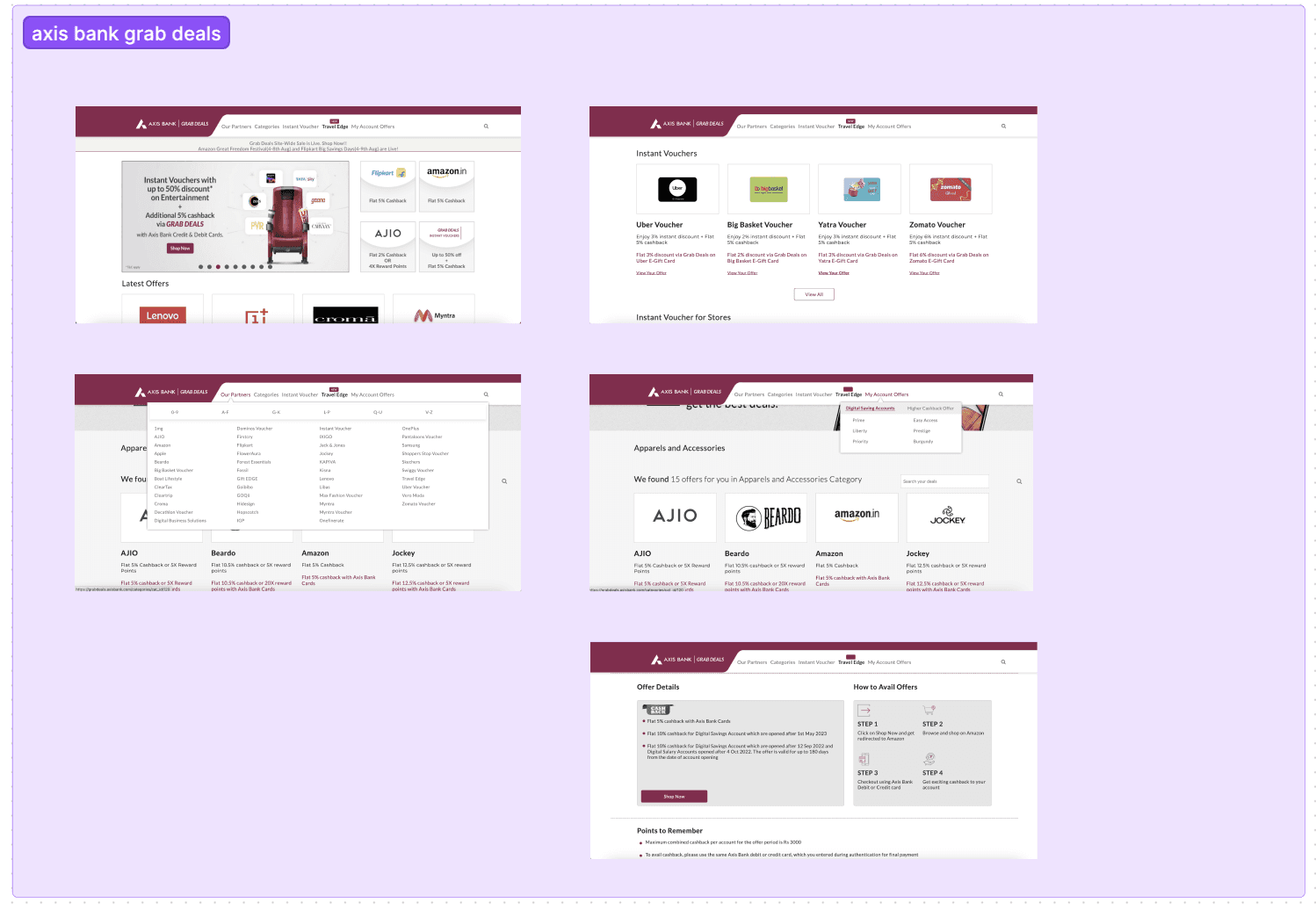

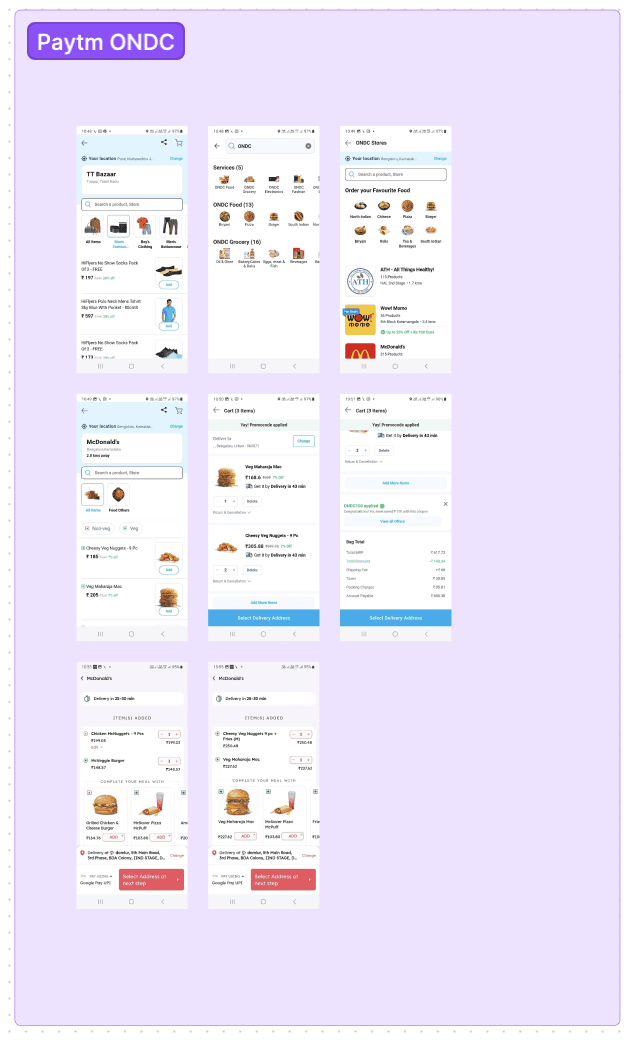

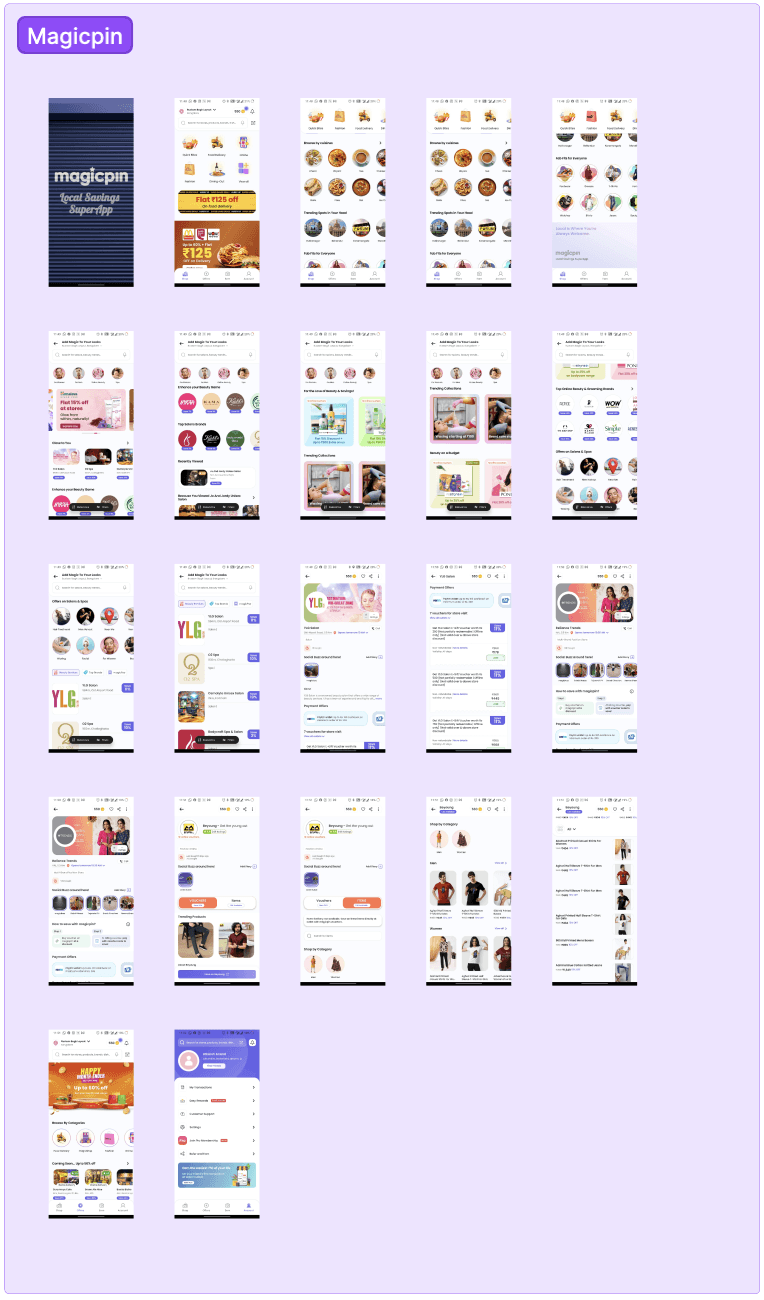

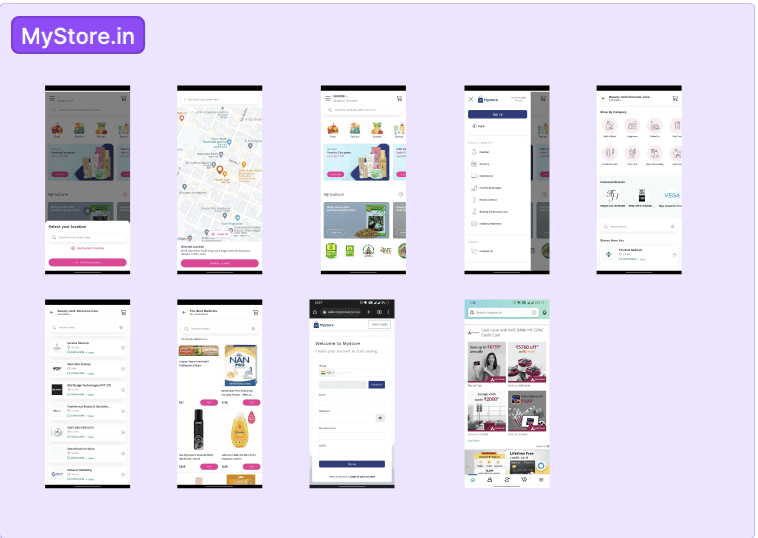

What competitors are doing?

We analysed Indian competitors like Tata Neu, Paytm, Jio, Cred as well as global players like Revoult, WeChat, Grab who are one stop shops

We explored various technology enablers like ONCD, Account Aggregators, Govt schemes

Business models of various companies offering one stop shopping solutions

Understand business model of Fintechs and startups like Bharatpe, that are venturing into lending business.

Mapping of the stakeholders

We mapped the various stakeholders that are involved

Stakeholder Mapping

DISTRIBUTOR/ WHOLESALER/ RETAILER

SBI

3rd party:

FINTECH(Tech Enablers), Delivery partners

END CUSTOMER

Seller

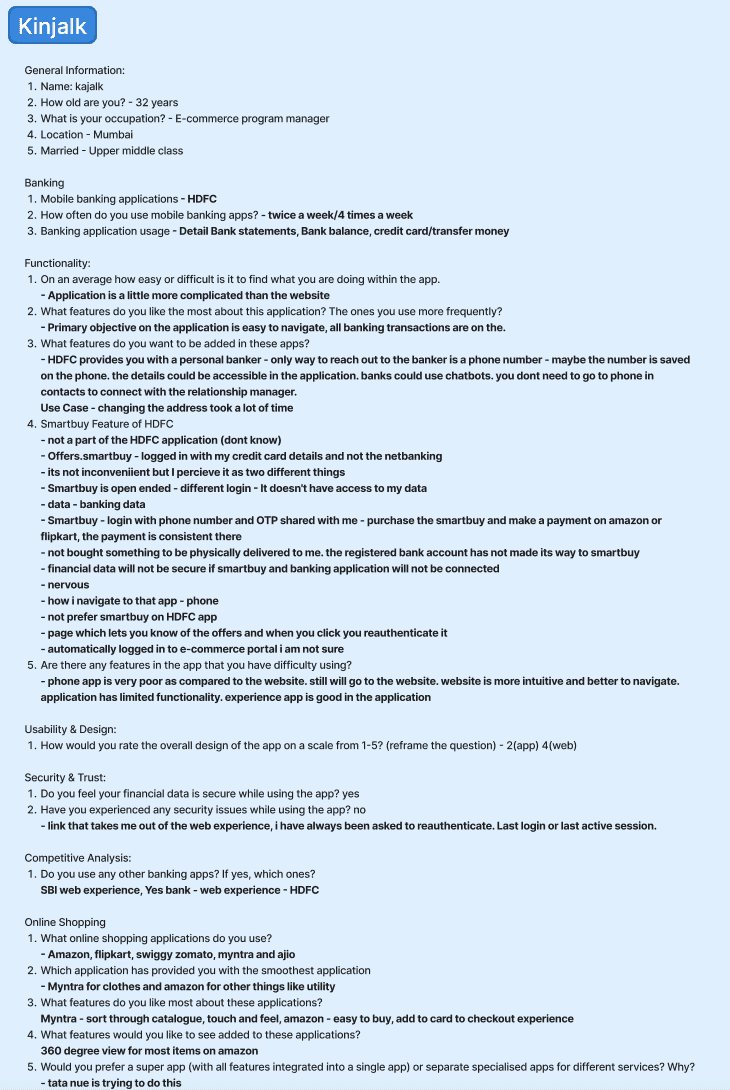

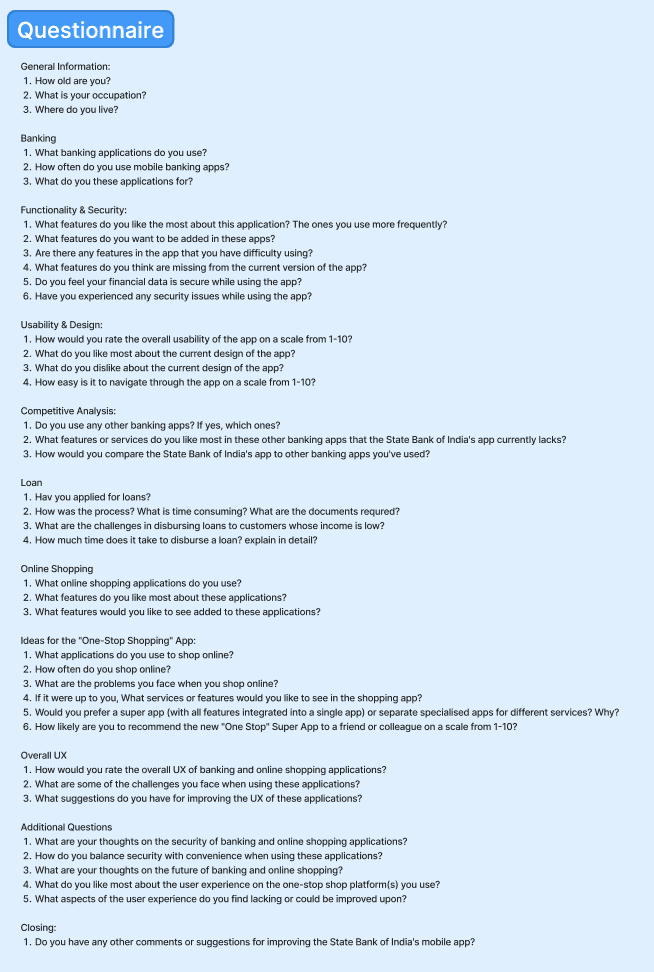

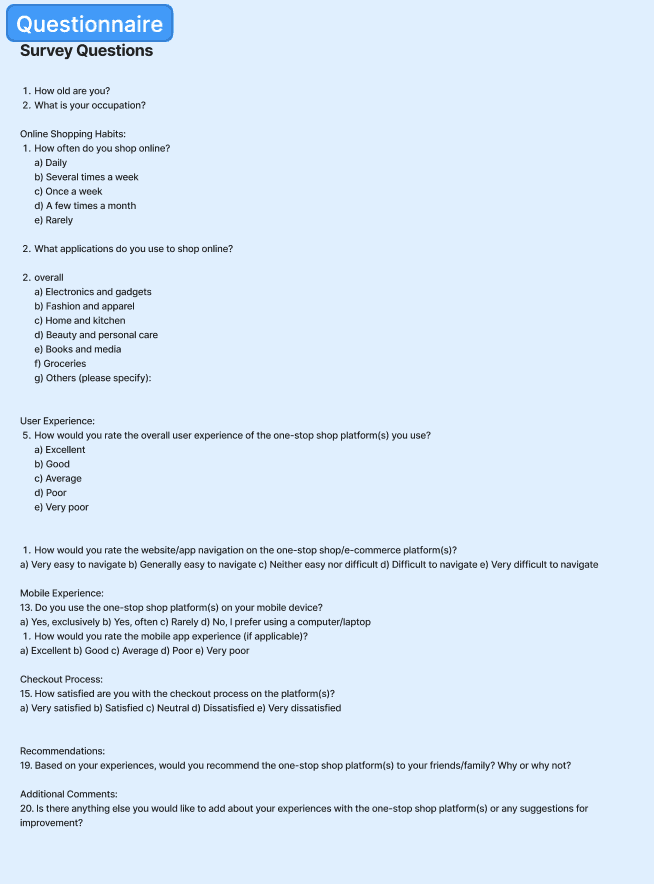

Primary research insight

In-person Interviews

12

Survey Responses

30

Around 60% of the surveyed users are either not aware or do not use the promotions and rewards offered through mobile banking applications. They prefer other Fintech apps.

Around 70% of the surveyed users are willing to use one stop solution app from their bank for online shopping from local stores given that the experience is seamless and secure.

Around 70% of the surveyed users prefer to shop online several times in a month.

For a superapp to work in India, it must first offer hyper-personalised and hyper-localised user experience and overcome users’ reliance on already existing apps, for example, Swiggy and Zomato, for food delivery.

Lack of credit history, inadequate collateral, lack of awareness about government schemes, and high-interest rates are some of the significant challenges faced by MSMEs in securing financing.

Banks have a target to give out loans to the right customers and sellers, but are not able to identify the right customers with adequate collaterals and good credit history.

What our secondary research says?

75% of global workforce

By 2025, Millennials and Gen Zs will comprise three-quarter of the workforce.

77% of India

1.10 billion active cellular mobile connections in India

48.33 Cr customers

SBI has max no. of total assets, loans, ATMs, Branches and deposits as compared to other banks.

65% will switch banks

Millennial and GenZs are ready to switch bank for a better tech platform

1/10 of the world's digital buyers will live in India this year.

82% will switch for personalised rewards

Millennial and Genzs are willing to switch banks for personalised rewards and offers.

90% bankers believe open-banking will boost their growth

bankers believe open-banking will boost their organic growth by 10% and reduce cost of customer acquisiton

33.5% CAGR

Indian digital lending companies is set to grow from USD 38.2 billion in 2021 to nearly USD 515 billion by 2030

Based on our secondary research we built some hypothesis on the one-stop shop, its need and usefulness. We validated our hypothesis based on the user interviews and survey responses we gathered from our target user groups.

Validating our hypothesis

Hypothesis

Insights

Customer wants to have one stop shop app for all their needs.

They prioritise convenience over security/safety

They like to compartmentalise and have a hyper-localised app to fulfil a specific need without compromising on seamless experience and security

MSMEs find it difficult to secure finance due to Lack of credit history, inadequate collateral, lack of awareness about government schemes, and high-interest rates from traditional banks

Lack of credit history, inadequate collateral, lack of awareness about government schemes, and Primary research insight are some of the significant challenges faced by MSMEs in securing financing.

Banks have a target to give out loans to the right customers and sellers, but are not able to identify the right customers with adequate collaterals and good credit history.

Banks have limited resources, pressure to meet lending targets and cannot always afford to do the due diligence necessary to fully assess the creditworthiness of every potential borrower.

Customers have to wait in long queues to speak to a bank representative, no clear information about the status of their account or process.

Customers have to wait in long queues due to understaffing, outdated technology, and a lack of training for bank staff

Customers are unable to redeem SBI reward points easily

Customers are unable to redeem SBI reward points easily due to technical glitch, high threshold, limited options and lack of awareness

The experience of the current traditional banking apps is generic, non-intuitive and glitchy as compared to the experience provided by challenger banks/fintechs

The perceived experience of the current traditional banking apps is generic, non-intuitive and glitchy as compared to the experience provided by challenger banks/fintechs

Seller

Seller

Bank

End Customer

End Customer

End Customer

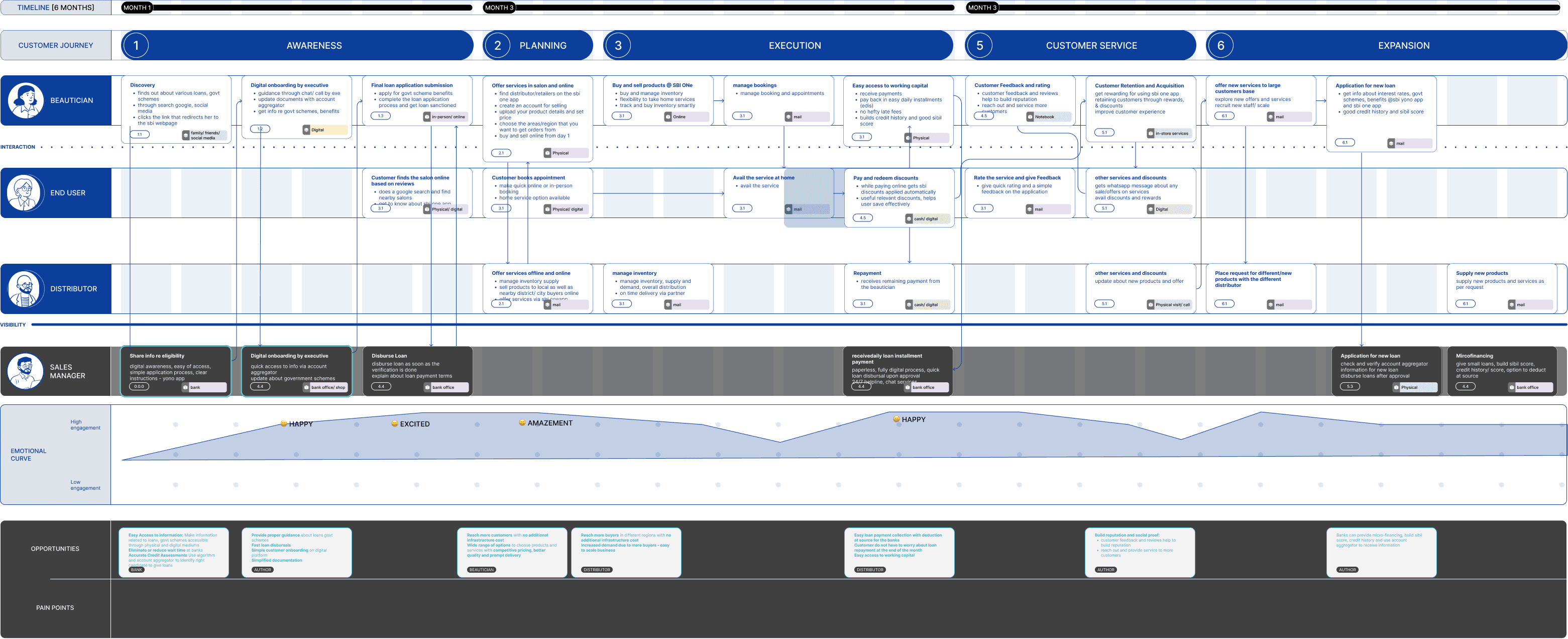

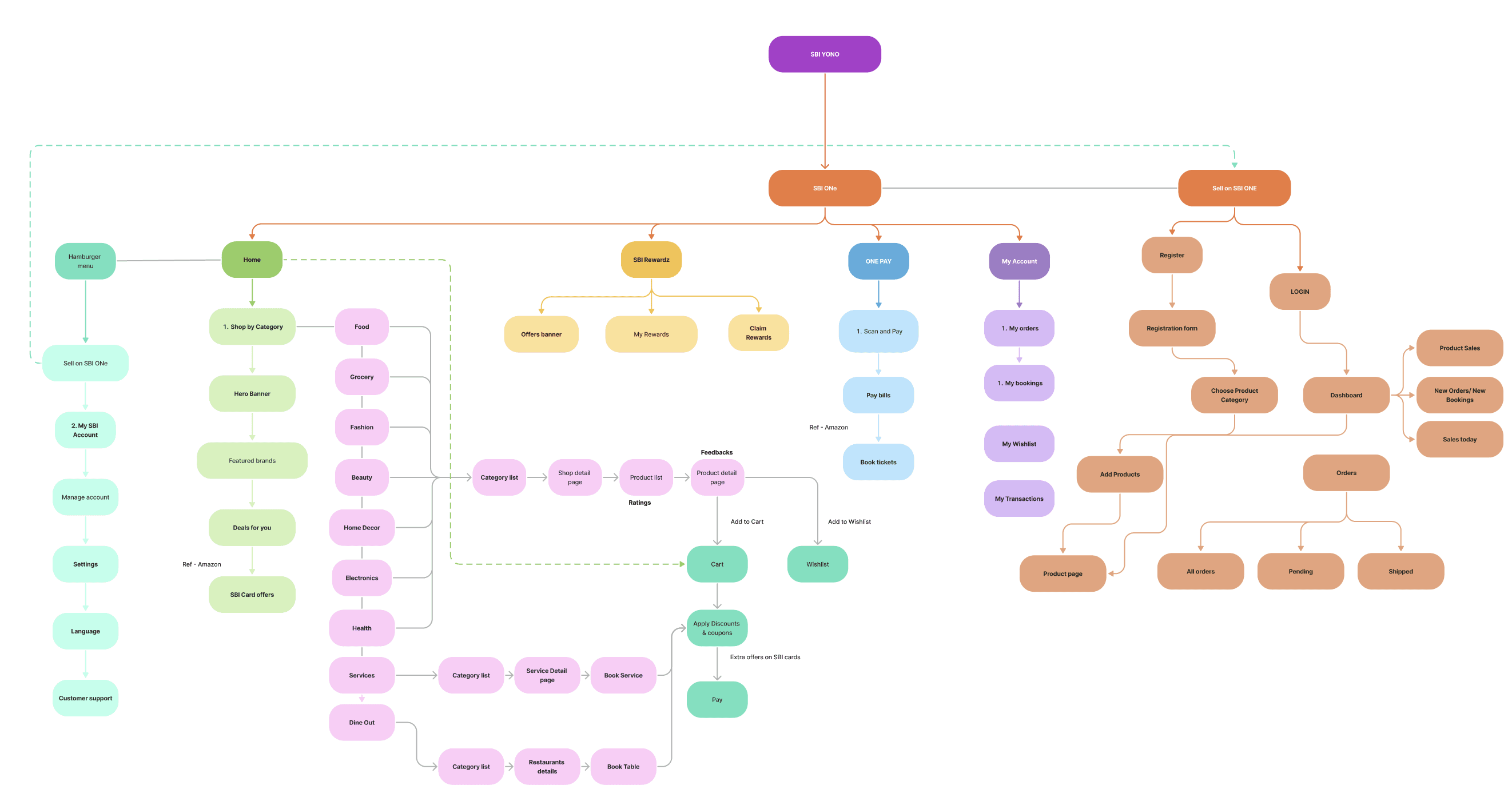

What could be the ideal journey?

Information Architecture

Based on the to be journey we ideated on the information architecture, which covers simplified user journey.

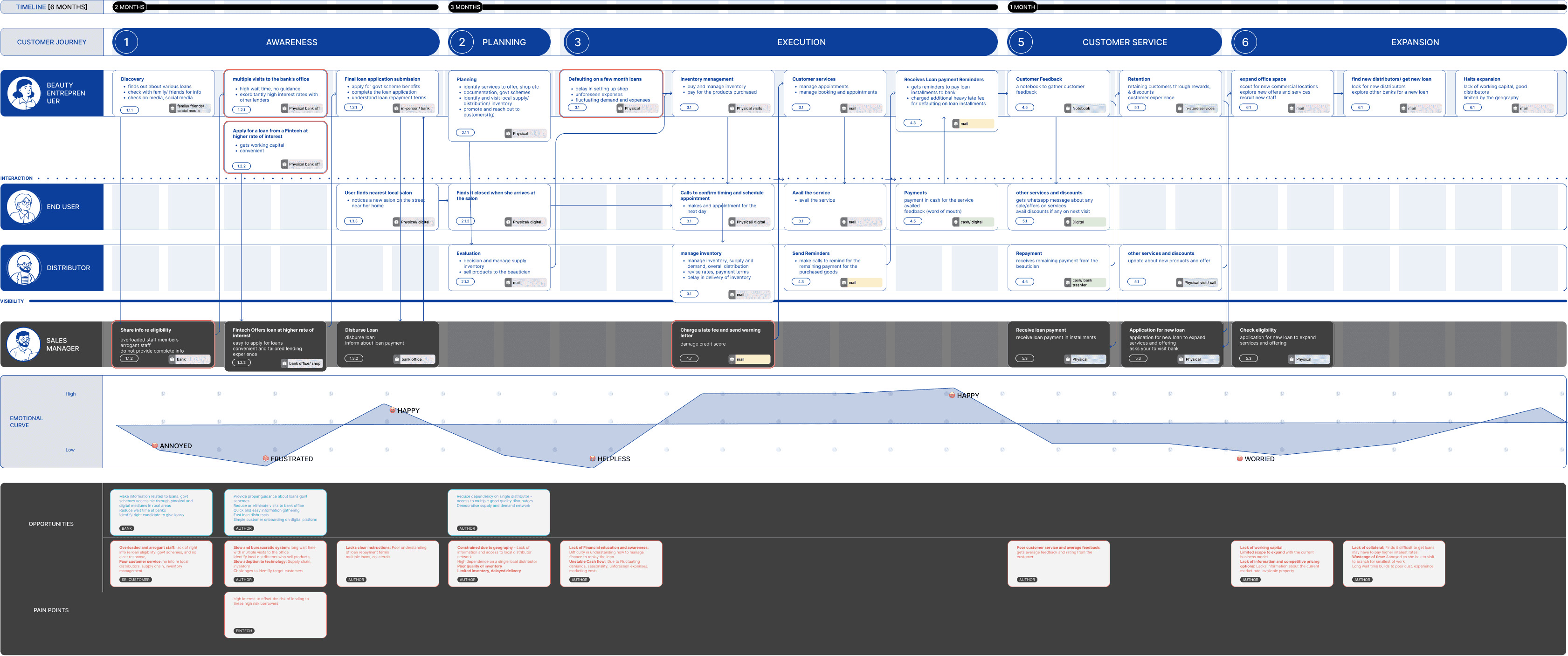

What is current situation?

In the current scenarios there are various one-shop stop present in the market, but most of the have their own dark stores and local vendor are not getting benefited from those apps, rather it is becoming difficult for local shops. Also there are very few apps which are providing all kinds of shopping and services at the moment.

Challenges

Fragmented Experience

They like to compartmentalise and have a hyper-localised app to fulfil a specific need without compromising on security

No access to affordable Loans

Lack of credit history, inadequate collateral, lack of awareness about government schemes, and high-interest rates are some of the significant challenges faced by MSMEs in securing financing.

Untapped Potential

Bank's customer engagement remains transactional. Customers have to wait in long queues due to understaffing, outdated technology, and a lack of training for bank staff

Limited Reach

Local businesses struggle to tap into the digital market effectively. Banks have limited resources, pressure to meet lending targets and cannot always afford to do the due diligence necessary to fully assess the creditworthiness of every potential borrower.

Coupon Hassles

Customers miss out on potential discounts due to scattered offers. Customers are unable to redeem SBI reward points easily due to technical glitch, high threshold, limited options and lack of awareness

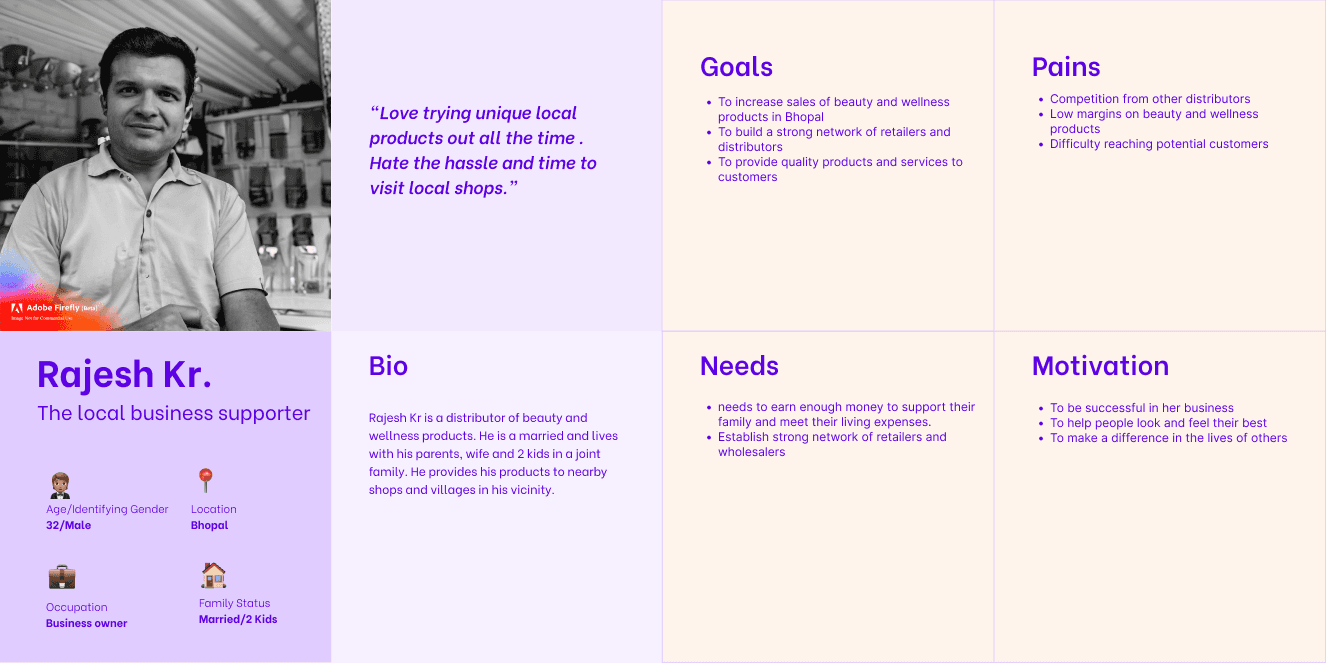

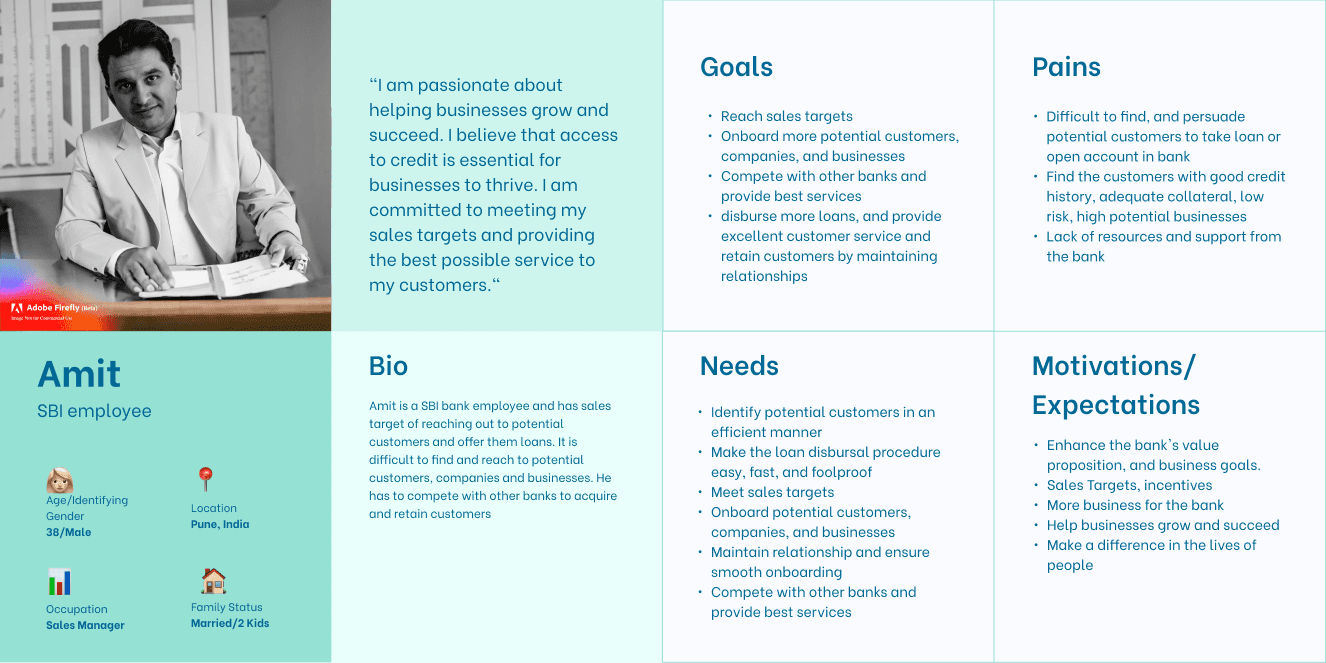

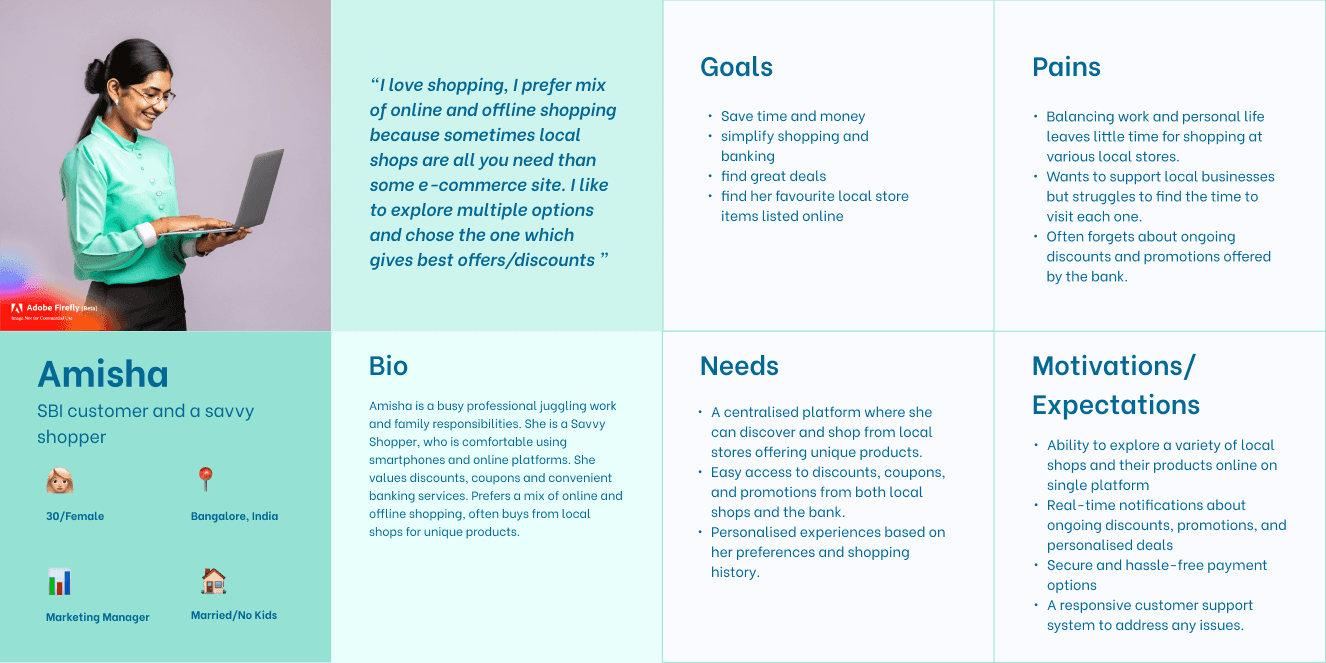

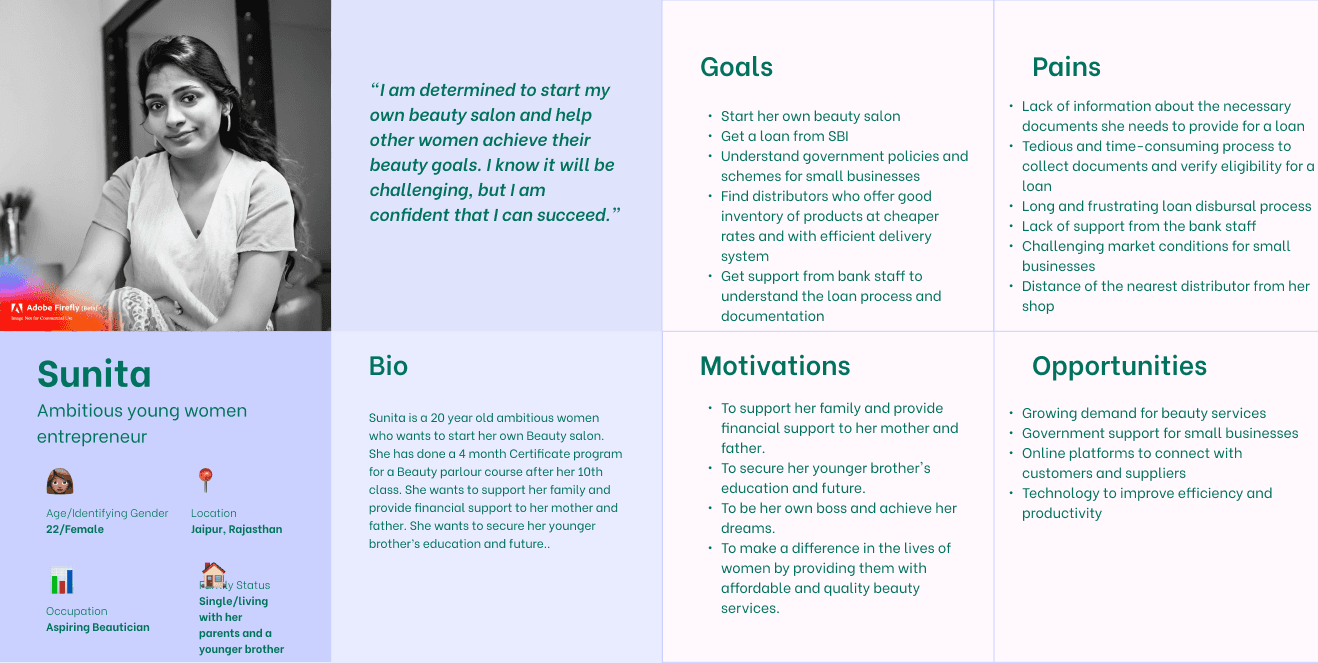

Based on our research we designed few personas for the one-stop shop application covering most of the stakeholders of the one-stop shop application.

Persona

Final Concept

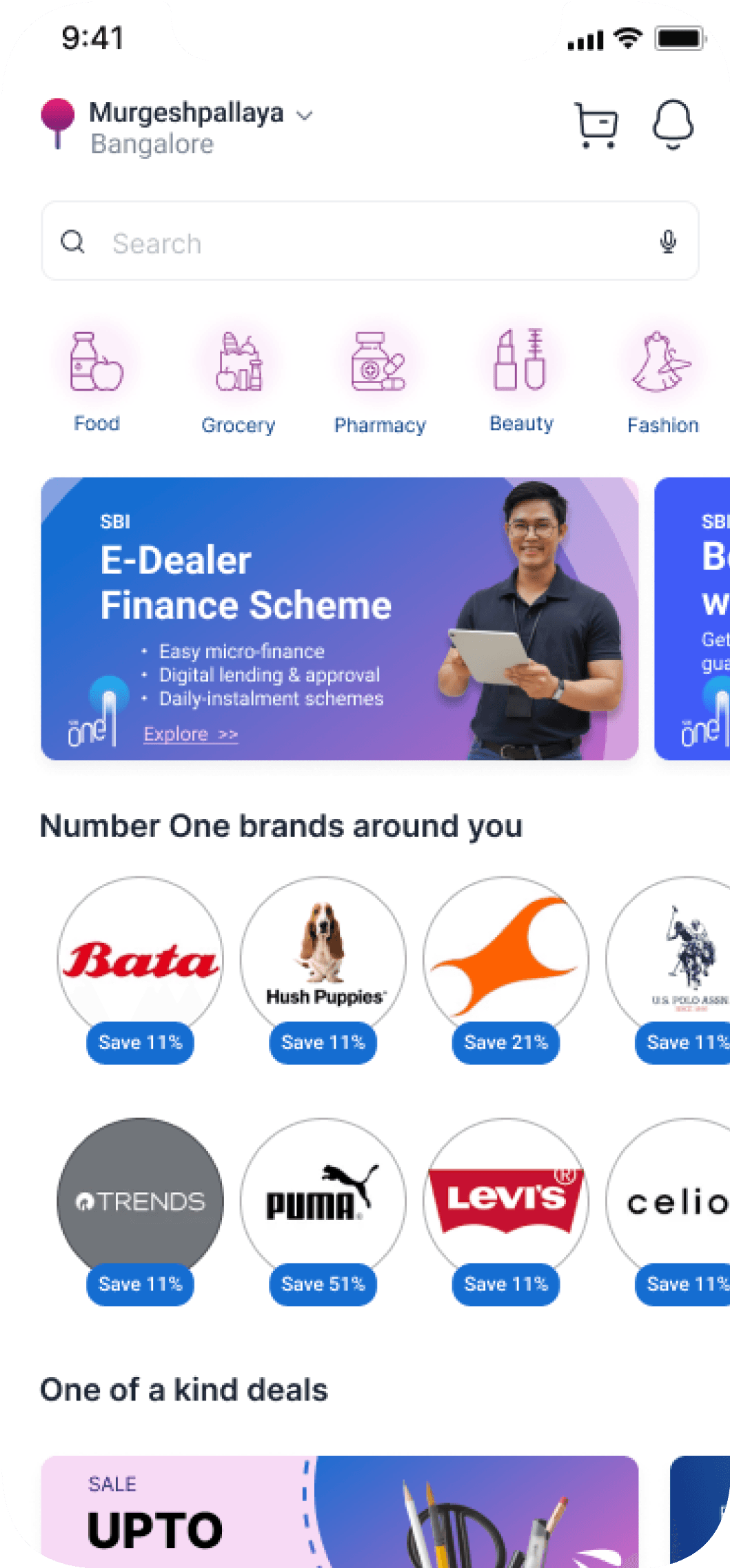

SBI One: The Future of E-commerce and Services

Introducing SBI One - a revolutionary aggregator platform built on the ONDC protocol. ONE stands for Open Network E-commerce. At its core, SBI One is an embodiment of the Open Network Digital Commerce vision, seamlessly blending the Open-banking model with the vast ONDC network and leveraging SBI’s expansive customer base.

Why Choose SBI One?

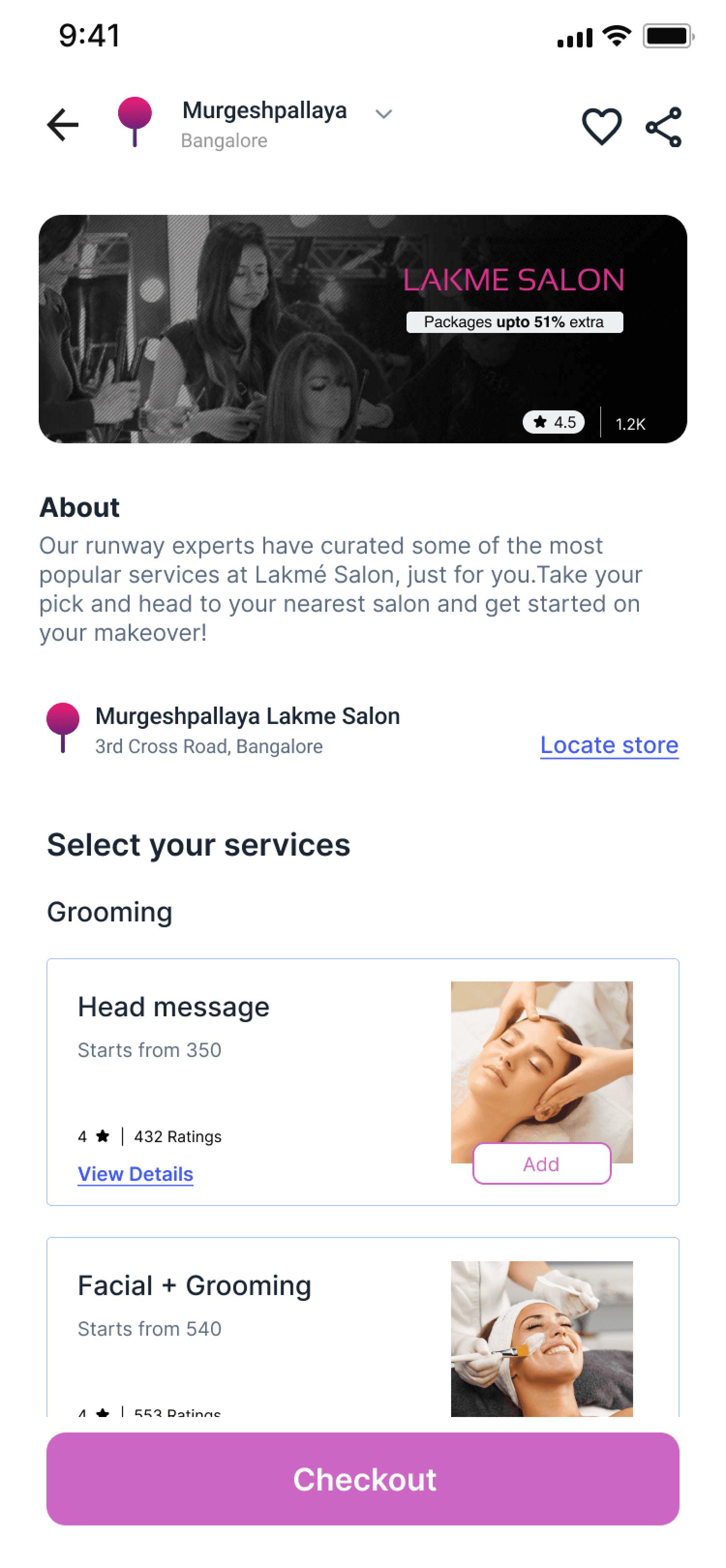

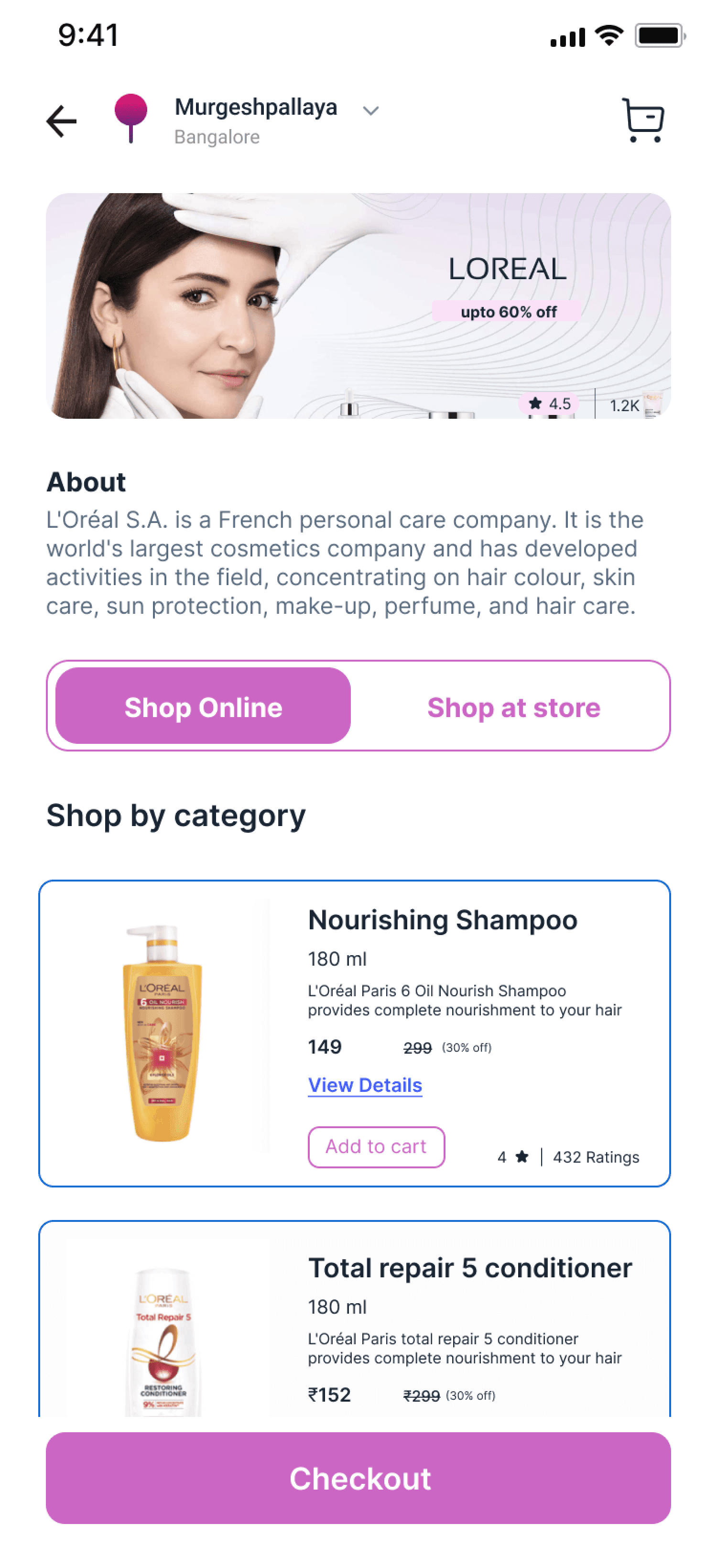

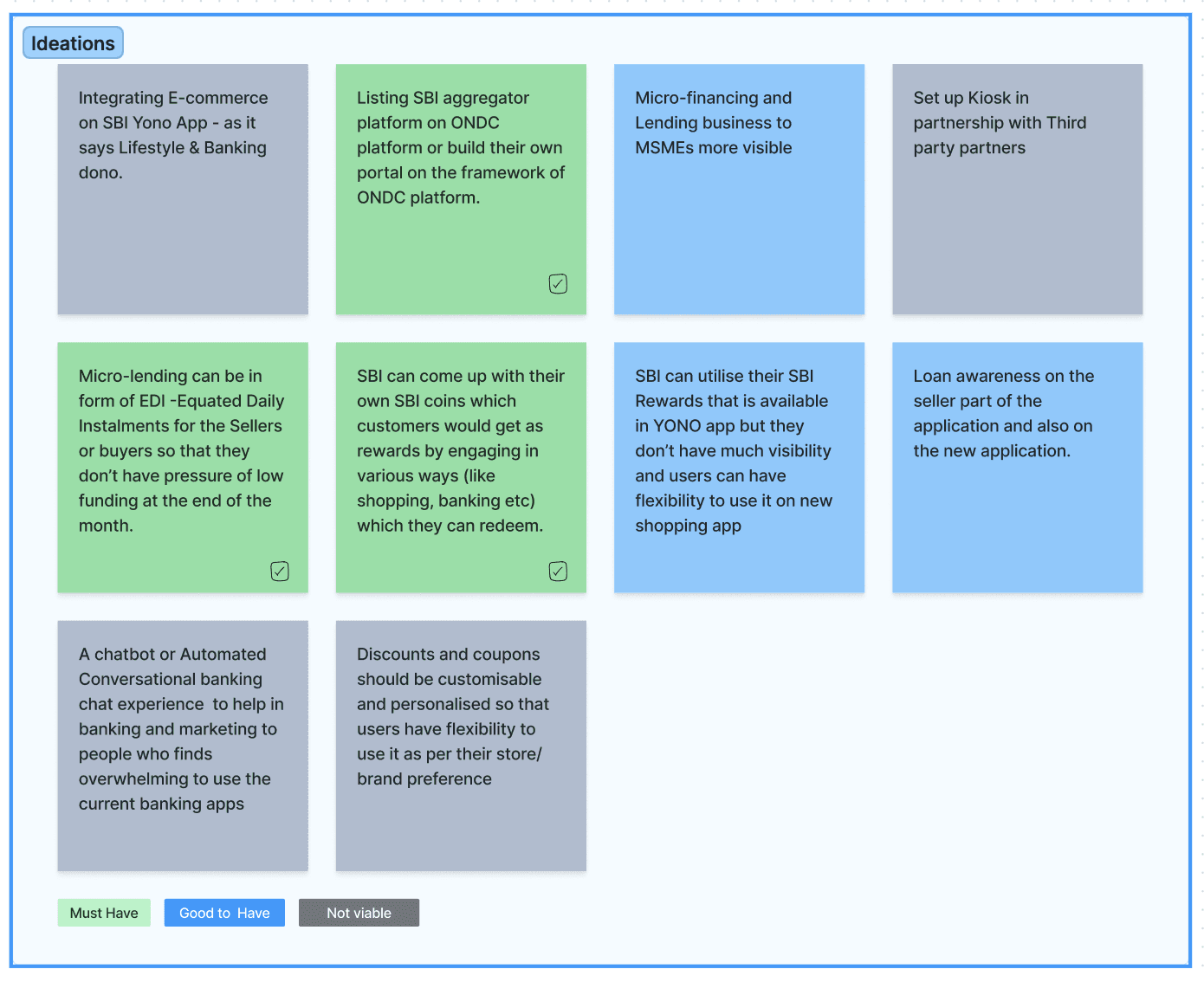

Diverse Offerings: Unlike traditional platforms that focus solely on products, we've expanded our horizons. From tangible products to unique services like beauty treatments, SBI One caters to a broader market.

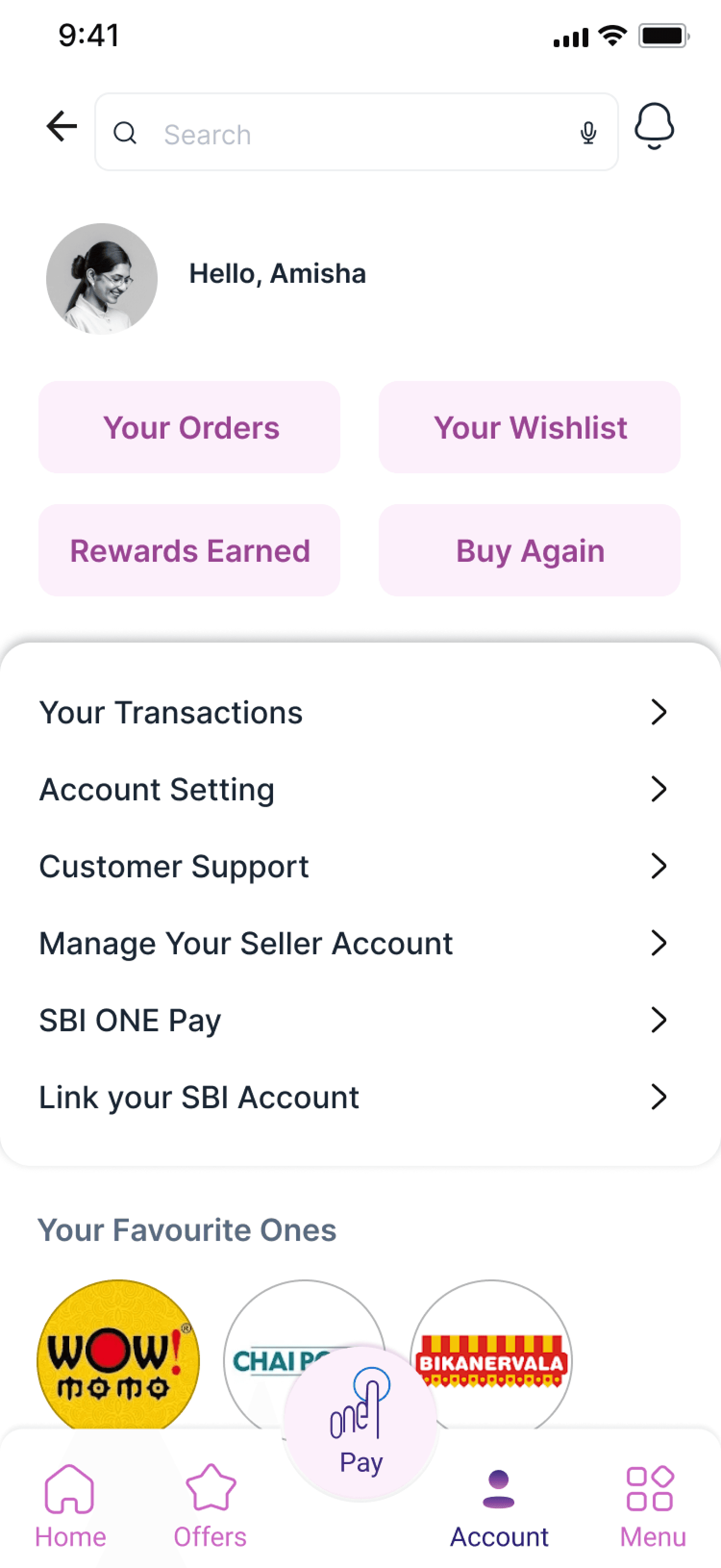

Empowering Users: Financial literacy and awareness is a cornerstone of our platform. Users gain insights into micro-lending, various SME loan schemes, Govt schemes and digital loan disbursement options (available via the existing SBI YONO platform) all through our dedicated SBI offers.

Innovative Payment Solutions: With our unique Equated Daily Instalments (EDI) system, businesses and end-users can opt for daily payments. This breaks the EMI norm, ensuring monthly financial commitments are more manageable.

Hyper-Local and Personalised: Once on the app, users are introduced to tailored options from local stores and services surrounding them, enhancing convenience and choice.

Rewards and Incentives: Earn as you shop with SBI One coin, a reward system with real monetary value. And for those who love traditional shopping, our app-provided coupons can be redeemed at participating physical stores.

Dedicated Seller Portal: We value our vendors. That's why we've launched an exclusive app for them, enabling business insights, product listings, and performance metrics, all at their fingertips.

Access SBI One effortlessly by one tap either through the established SBI YONO app or by downloading it from app stores. Dive into a comprehensive shopping and service experience designed for the modern user. Join us in redefining commerce!

Business Process Diagram

SBI

SBI One App

Third-Party Partners, NBFC, Fintech

Enable faster, hassle-free loan disbursals

Equated Daily Installments for Loan Repayment

Onboarding new customers and business

partner with third party companies

24/7 Guidance and support

Accurate Credit Assessments

Automatically applies SBI discounts, enhancing customer savings.

Buying and selling online powered by ONDC

Build better credit and SIBIL score

NEW BUSINESS

beauty entrepreneur

beauty entrepreneur

END user

(sbi customer)

DISTRIBUTOR/ WHOLESALER/ RETAILER

SBI Relationship and Support team

Account Aggregators

SBI Rewards

Ideations

It is always about the team work!!!

Prospective Impact

For Users:

Enhanced Shopping Options: Users have a richer shopping experience with a vast array of both products and services, from buying a gadget to booking a beauty service.

Financial Empowerment: By providing insights into micro-lending and SME loan schemes, users are better informed and positioned to make wise financial decisions.

Flexible Payments: The innovative EDI system offers an alternative to traditional EMIs, potentially reducing financial stress for many.

Local Connection: Hyper-localized options mean users can discover and support businesses in their own neighborhoods, thereby fostering community connection.

Monetary Benefits: The rewards system offers tangible benefits, encouraging more frequent shopping, and the integration of physical store coupons maintains a bridge to traditional retail shopping.

For Businesses:

Market Expansion: By being on an aggregator platform like SBI One, businesses can tap into SBI’s massive customer base, potentially leading to increased sales and revenue.

Service Inclusion: Service-oriented businesses, which might have felt left out on traditional e-commerce platforms, now have a platform to shine.

Financial Tools Access: Especially for SMEs, the insights and tools related to micro-lending and other financial schemes can be invaluable.

Enhanced Customer Engagement: The hyper-local feature ensures businesses can target and engage with local customers more effectively.

Reward Collaborations: The chance to be part of SBI One's reward ecosystem can act as an incentive for businesses to offer better deals, leading to increased user engagement and loyalty.

Thank you

Back